par Francois de Siebenthal | Fév 11, 2013 | Uncategorized

Le pape Benoît XVI a annoncé lundi sa démission. Le pape Benoît XVI a annoncé lundi sa démission à partir du 28 février, dans un discours prononcé en latin lors d’un consistoire ordinaire au Vatican, a confirmé le porte-parole du Saint-Siège. “Le pape a...

.jpg)

par Francois de Siebenthal | Fév 11, 2013 | Uncategorized

Chers compatriotes,Chers amis, Je me souviens….. Je me souviens lorsque nous avons fondé l’UDC, c’était il y a 12 ans !! Je me souviens de la réprobation des médias, des autres partis qui nous traitaient de tous les noms d’oiseaux, nous...

par Francois de Siebenthal | Fév 8, 2013 | Uncategorized

Ateliers Monnaies complémentaires Soumis par Camille le ven, 01/02/2013 – 16:40 Publié dans Evénements EcoAttitude Monnaies complémentaires La monnaie est au coeur de tous les problèmes que traverse notre société. La monnaie dont la fonction première était de...

par Francois de Siebenthal | Fév 8, 2013 | Uncategorized

La croisade du Coluche italien L’humoriste Beppe Grillo, leader du “Mouvement cinq étoiles”, récolte 15% des intentions de vote en Italie, l’équivalent d’une centaine de sièges. Cela rappelle le score de Coluche, lors de la...

par Francois de Siebenthal | Fév 8, 2013 | Uncategorized

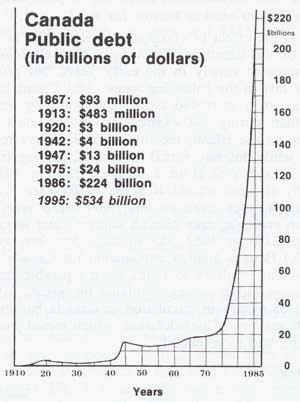

They say, interest rate was never so low, but In fact, it is a big lie because the interest rate is going to infinity… Why ? Because they create the capital in an unlimited way out of nothing,then, if you create an infinity of capital, the interest rate becomes...

Commentaires récents