par Francois de Siebenthal | Avr 15, 2017 | Uncategorized

Présidentielle: un “bug” fait des milliers de doublons de cartes électoralesAu moins 500 000 électeurs sont inscrits deux fois sur les listes électorales, la plupart à la suite d’un déménagement. Mais attention: le double vote est interdit et...

par Francois de Siebenthal | Avr 15, 2017 | Uncategorized

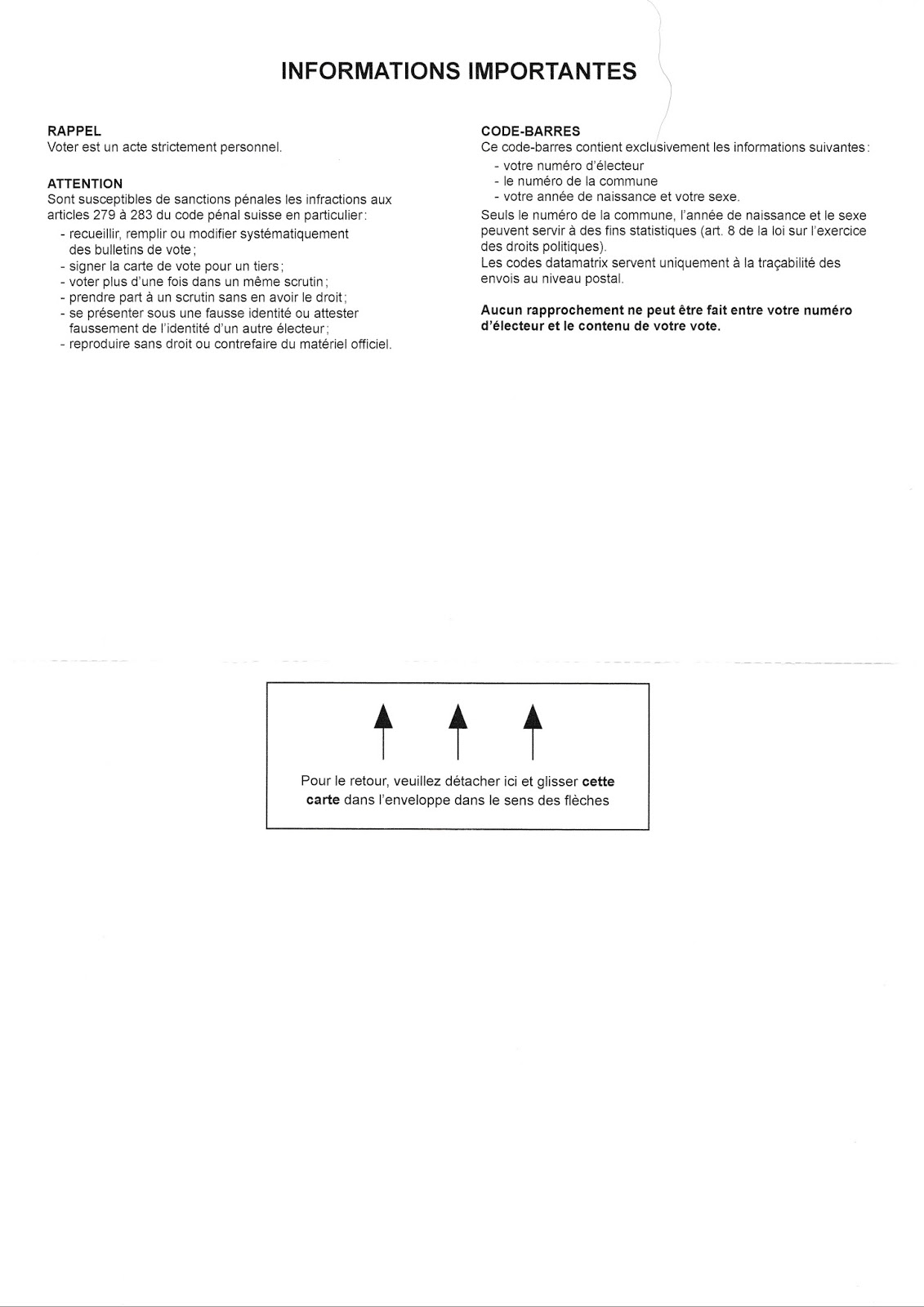

Exemples: Il est écrit ci-dessous dans la photo tout en bas : “Aucun rapprochement ne peut être fait entre votre numéro d’électeur et le contenu de votre vote …. ” Faux: URGENT Le principal danger contre notre démocratie, c’est le...

par Francois de Siebenthal | Avr 13, 2017 | Uncategorized

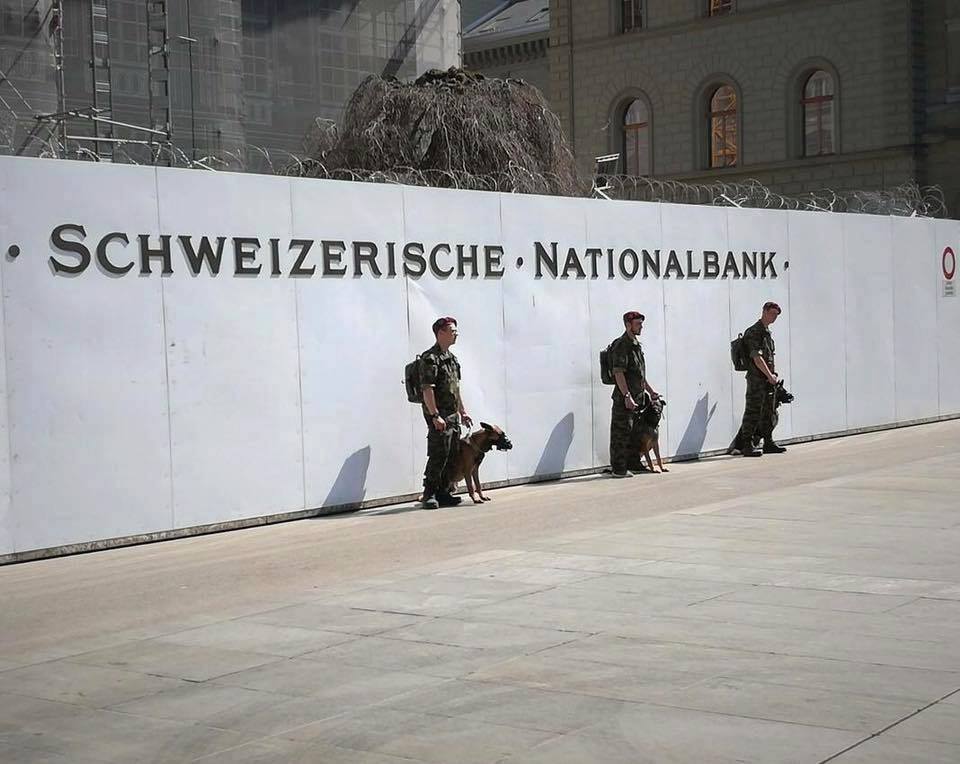

La BNS sous haute protection ! L’argent pour les armes tue… http://www.rts.ch/info/economie/8531989-comment-des-tirs-de-missiles-en-syrie-profitent-a-la-banque-nationale-suisse.html Comment des tirs de missiles en Syrie profitent à la Banque nationale...

par Francois de Siebenthal | Avr 13, 2017 | Uncategorized

M. Asselineau contre le Tamiflu et Mme R. Bachelot qui a dépensé près de 2 milliards d’Euros, sic… Des enquêtes doivent être menées contre ceux qui provoquent des grandes peurs collectives, notamment contre les laboratoires pharmaceutiques qui profitent...

par Francois de Siebenthal | Avr 12, 2017 | Uncategorized

En rouge: Geld für Waffen tötet L’argent pour les armes tue ( notamment l’argent de la BNS dans les armes, y compris nucléaires aux USA ) La BNS sous haute protection ! L’argent pour les armes tue...

Commentaires récents