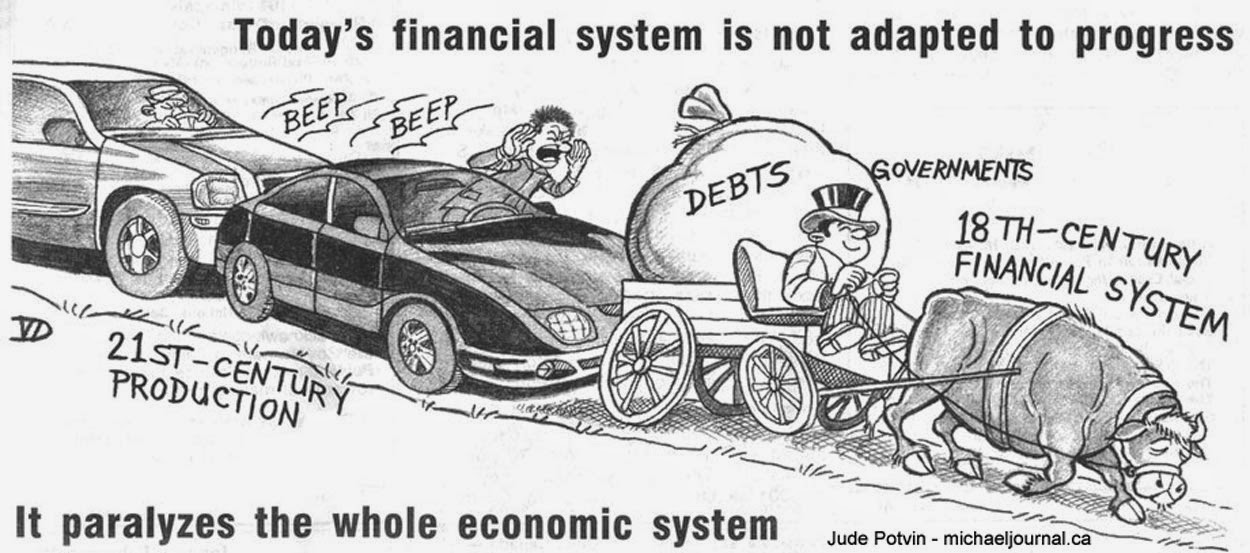

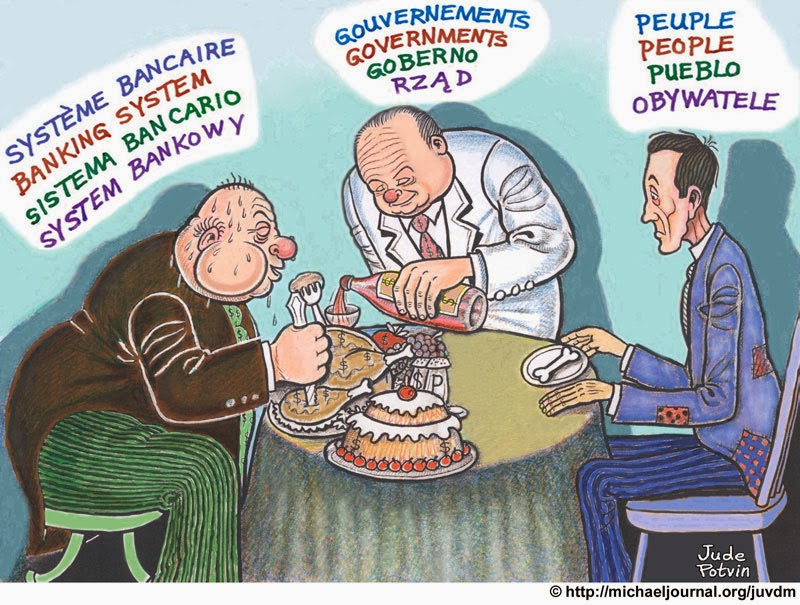

The love of money is the root of all evil.

The Vatican and IOR, see the report below, are not following the encyclical Vix pervenit.

Roma locuta, causa finita… Rome has spoken, the cause is closed… Any rate of interest kills millions of human beings…

Explanations:

https://vimeo.com/136794177

http://www.papalencyclicals.net/Ben14/b14vixpe.htm

https://en.wikipedia.org/wiki/Vix_pervenit

http://www.ior.va/content/dam/ior/documenti/rapporto-annuale/IOR-Annual%20Report%202016.pdf

Invitations 2017

In English

23, Av. Edouard Dapples, CH 1006 LAUSANNE. SUISSE

Tél: international ++ 41 21 616 88 8

http://desiebenthal.blogspot.ch/2015/12/swiss-positive-money-social-credit.html

François de Siebenthal: The love of money is the root of all evil.

3 mai 2009 – Jesus said that the love of money is the root of all evil. This had no meaning for me (although I thought it did) until I read and studied the Social …

François de Siebenthal: Money creation management by the Swiss …

9 oct. 2013 – At least, the SNB controls and limits the money creation and the profits are … Be praised, my Lord, through those who forgive for love of you; …

François de Siebenthal: Games to explain money sytems

25 déc. 2016 – You know that money is created in the form of debts with interest ….. It is really a way to avoid this love of money which is the root of all evils.

The love of money is the root of all evil.Social credit is a solution …

7 févr. 2017 – François de Siebenthal: Games to explain money sytems … 2016 – It is the love of money that is the root of all evil, and with this system, there is …

François de Siebenthal: Federal Council adopts monetary policy report

23 déc. 2016 – He recently spoke to Francois de Siebenthal, who is a former banker from ….. Helicopter Money: Or How I Stopped Worrying and Love …

|

||||

|

ANNUAL

REPORT 2016

Istituto per le Opere di Religione

Cortile Sisto V

00120 Vatican City State

Vatican City State

Registered under No 1 in the Register of Legal Persons

held at “Governatorato” of Vatican City State

Authorization n. 1 of 10/07/2015 issued by AIF,

to carrying out on a professional basis financial activities at Vatican City State

digital copy on site www.ior.va

“Money must serve,

not rule.”

His Holiness Pope Francis, Evangelii Gaudium, 2013

5

TABLE OF CONTENTS

PRESIDENT OF THE COMMISSION OF CARDINALS’ MESSAGE 7

PRELATE’S MESSAGE 8

MANAGEMENT REPORT 9

CHAPTER 1. STRATEGIC INFORMATION 11

1. President of the Board of Superintendence’s Message 11

2. Mission, Customers and Services 13

3. Corporate Governance 14

4. IOR Organization Chart 21

5. Regulatory Framework and Tax Requirements 21

6. Proposal of Distribution of the Net Profit For the Year 26

CHAPTER 2. OPERATIONAL INFORMATION 27

1. 2016 Business Review 27

2. Forecast for 2017 28

FINANCIAL STATEMENTS 31

Balance Sheet 33

Income Statement 34

Statement of Comprehensive Income 35

Statement of Changes in Equity 35

Cash Flow Statement 36

Explanatory Notes 38

Part 1. Accounting Policies 38

Part 2. Information on the Balance Sheet 61

Part 3. Information on Income Statement 82

Part 4. Information on Comprehensive Income 92

Part 5. Information on Risks and Hedging Policies 95

Part 6. Information Concerning Equity 119

Part 7. Related Party Transactions 123

REPORT OF THE REVISORI 125

REPORT OF THE EXTERNAL AUDITORS 131

The present Annual Report has been translated from the original one which is prepared in Italian

IOR

Annual report 2016

7

PRESIDENT OF THE COMMISSION OF CARDINALS’ MESSAGE

The presentation of an annual report provides a convenient opportunity to do a double internal

examination. The first one relates to the last year and the second one refers to the current year, or

better, the future years.

It seems to me that this rule can be applied to the presentation of the IOR annul report for the year

2016. In it, like every human work, one can find anxieties of great success, overcoming complex

or inherited situations, To offer a service appropriate for everyone’s mission, personal contribution

to a cause that is worth serving for professional reasons or for high ethical, religious or humanitarian

inspiration. I think this can be behind the figures presented in the IOR 2016 annul report.

But along with the best dispositions and personal efforts, there is also the stubborn realities of global

economic and financial performance and the recurrent volatility phenomena that often complicate

predictions and expectations.

In this complex context, during the year 2016, the effort of all the members of the large family of

IOR, ecclesiastical or laity servants, each in its place of responsibility at the various levels, took place.

But they come together to serve a global cause with that ethical and exemplary sense that the Holy

Father rightly claims from us all and from each of us. This is His first directive and first requirement,

and not efficiency at any cost.

In this line, as President of the Commission of Cardinals, I feel the duty to express the most heartfelt

thanks to the Cardinals, the Prelate, the Board Members, the Directorate, the Revisori and the

whole staff of our Institute. Allow me to remind all of us that the Holy Father, as he has clearly indicated

on several occasions, requires competent and effective collaborators, but always guided by

inalienable ethical principles, both inside and outside, as servants of the Church. It is our duty to

continue to improve our services in the years to come.

IOR

Annual report 2016

Cardinal Santos Abril y Castelló

President of the Commission of Cardinals

Istituto per le Opere di Religione

8

PRELATE’S MESSAGE

I wish to add my own to the authoritative voices of the Cardinal President of the Commission of

Cardinals’, the President of the Institute and the Director General simply to express my thanks to

all those who, through their commitment and work, have over the past year contributed to renewing

the way the Institute operates. Thanks to them, one step at a time, the IOR has increasingly

been becoming an entity that serves the Church straightforwardly and in a humble way, aware of

its importance in connection with supporting the Holy See’s and Catholic religious organisations’

practical activities, and developing a conscience whereby the Institute is no longer viewed almost

as a separate and independent entity but rather as one that takes as the reason for its very existence

its subordination to projects targeted only to the real needs of Catholics works and not to making

money for the sole purpose of making money. If thanks to management centred on Catholic social

ethics there is money, that is positive, and if for whatever reason at times there is less than expected,

never mind. The Lord will always lend His support to those who trust in Him: even “re oeconomica”.

In these days of Easter, the people who work in our Institute ought to reflect upon the words Pietro

said to the lame man: “Silver or gold I do not have, but what I have I give you: in the name of Jesus

Christ of Nazareth, get up and walk!” (Acts 4-6). So we must go forward bravely, without ever

forgetting that there is One above us who guides events and this should give us confidence but also

a great sense of responsibility.

IOR

Annual report 2016

Msgr. Battista Mario Salvatore Ricca

Prelate

Istituto per le Opere di Religione

MANAGEMENT REPORT

11

CHAPTER 1

STRATEGIC INFORMATION

1. PRESIDENT OF THE BOARD OF SUPERINTENDENCE’S MESSAGE

Sinceits appointment in July 2014, the Board of Superintendence has worked on the necessary transformation

of the IOR to serve with Prudence the Holy Father in fulfilling his mission as Universal

Pastor. This meant focusing on the nature and the quality of services offered to clients and to

the Church in a complex financial environment, the establishment of a framework with stronger

and clearer governance principles, strict compliance with applicable laws and regulations including

anti-money laundering procedures, the improvement of internal controls and risk management,

the execution of tax agreements with the United States of America and Italy, and the review of legal

issues in coordination with the appropriate Vatican authorities.

In 2016, the IOR has continued to make progress in rolling out the reform plan agreed upon by

the Board, supported by the new Directorate and the work of all its employees. In doing so, the

Board has given consideration to the words of the Holy Father regarding its particular responsibility

and particularly “the responsibility of guiding the institute’s strategic development in accordance

with its mission to serve, the Board should never lose sight of the ethical dimension of the choices

made in providing strategic guidance, recognizing that ethics is first and foremost in governing the

IOR, and may never be subordinated to profit, nor open to compromise”.

Collaboration between the Board and the Directorate

According to the Statute of the IOR, the Board has approved the business plan for 2016 which was

the continuation of the 2015 plan with a core focus on ethics and customer satisfaction and has

assisted the Directorate in its execution. It included the need to address the quality, reliability and

sustainability of investment solutions offered as well as the technical support offered to IOR client

base.

In addition, the Board has worked with the directorate towards strengthening the overall organization

including:

1. Ensuring compliance with law XVIII and Regulation No.1;

2. Strengthening the control functions with clearer governance principles;

3. Addressing human resource issues, such as increasing staff training, strengthening internal communication,

and hiring appropriate resources;

Jean-Baptiste de Franssu

President of the Board of Superintendence

Istituto per le Opere di Religione

IOR

Annual report 2016

12

4. Consolidation of the IT infrastructure;

5. Revising and strengthening the existing governance policy where necessary;

6. Continuation of the efforts of building new relationships with Italian banks, particularly in

the context of the tax agreement with Italy;

7. Continuing to reduce administrative costs, including dependency on outside consultants;

8. Developing a Risk Appetite Framework (RAF) for the IOR and reinforcing the risk-sensitive

approach and the Catholic investment criteria in the investment process as to strengthen the

quality of its products;

9. Addressing legacy issues to which IOR is exposed in coordination with the Vatican regulator

and judicial authorities.

Significant efforts were also made to allow the IOR to be FATCA compliant and, in addition, in

October, the Agreement between the Government of the Republic of Italy and the Holy See on tax

matters became effective. Both of these events represented a major milestone for the IOR and are

a very important step in all the efforts made to bring full transparency in the operations of the IOR.

The Board, after meeting with the Revisori and the external auditors, approved the Institute’s accounts

and the management report for 2016, ensuring compliance with applicable requirements

and new recommendations introduced by the AIF.

The net result for 2016 is Euro 36 million. This results – whose details are provided in “Financial

Statement” Section – reflects the continuous down trend of interest rate in Europe and the conservative

approach that the Institute has adopted on managing its assets since 2014. As described in

Management Report, Section 2, Part 1 – 2016 Business Review, this was achieved in a year of complex

financial and political evolutions.

In the meeting of the Board of Superintendence on 26 April 2017, attended by both the members

of the Revisori and the external auditors, the financial statements for 2016 and the proposed distribution

of profits to be made to the Holy See for 2016 were discussed and approved. As per the

Statutes these informations were provided to the Commission of Cardinals to enable them to decide

on the allocation of profits. The financial statements, prepared in accordance with IFRS, as

adopted by the Circular issued by the AIF, have been audited by Deloitte & Touche S.p.A.

2017 and beyond

All the efforts lead by the Board since 2014 will continue in 2017. Improving client experience at

IOR, working towards full compliance with AIF regulations, continuing its commitment to AntiMoney

laundering, working on the evolution of certain aspects of the IOR’s business model, developing

IOR’ approach to faith investing, furthering the work on governance, and consolidating

the role of the control functions will represent the Board’s main objectives.

Acknowledgements

I would like to thank all the Board members for their support, their contribution and their dedication.

Many of them have devoted a considerable amount of their time to help guide the IOR

through this year of transition and change.

In 2016, the Board has continued to strive towards building a close working relationship with the

Commission of Cardinals. I wish to extend my gratitude to the president and all the members for

their availability and support.

I also wish to express my appreciation for the work of Gian Franco Mammì, the Director General,

the Prelate Mgr. Ricca and to all employees of the IOR.

The work performed by the members of the Revisori and the external auditors have also been critical

to the progress made by the IOR.

IOR

Annual report 2016

13

2. MISSION, CUSTOMERS AND SERVICES

Mission of the Institute

The Istituto per le Opere di Religione (the “Institute” or “IOR”) is an institution of the Holy See,

founded on 27 June 1942 by Chirograph of His Holiness Pius XII. Its origins date back to the

“Commissione ad Pias Causas” established by Pope Leo XIII in 1887.

The mission of the IOR, established by its Statute, with reference to the Chirograph dated 1 March

1990 of His Holiness John Paul II, is “to provide for the custody and administration of goods transferred

or entrusted to the Institute by natural or legal persons, designated for religious works or charity.

The Institute can accept deposits of assets from entities or persons of the Holy See and of the

Vatican City State”.

The IOR strives to serve the global mission of the Catholic Church through the administration of

the entrusted assets and providing payment services to the Holy See and related entities, religious

orders, other Catholic institutions, clergy, employees of the Holy See and the accredited diplomatic

bodies.

The IOR is exclusively located on the sovereign territory of the Vatican City State and subject to

the regulations and legislation applicable therein. The IOR is supervised and regulated by the “Autorità

di Informazione Finanziaria” (AIF).

Customers of the IOR

Customers served by the Institute include:

a) Institutional counterparties (Sovereign Institutions of the Holy See and Vatican City State and

related entities, nunciatures and apostolic delegations, embassies and diplomats accredited to

the Holy See);

b) Non-institutional counterparties (Institutes of Consecrated Life and Societies of Apostolic Life,

Dioceses and other Vatican legal canonical or civil entities as legal persons; clerics and members

of Institutes of Consecrated Life and Societies of Apostolic Life, employees and retirees

of the Vatican as natural persons).

Most of the IOR’s clients are active in missions or perform charitable works at institutions such as

schools, hospitals or refugee camps.

The Catholic Church, through its institutions involved in missionary activities and charitable works,

is present throughout the world, even in countries with very basic infrastructure and underdeveloped

banking and payment systems.

In such cases, the IOR’s services are particularly valuable. For customers located in these areas, the

IOR is a bedrock, affirming itself as a trusted institution able to provide on-site services otherwise

lacking or absent. This is even more evident in those geographic areas with high political financial

instability.

Nature of the Institute’s services

On behalf of its clients, the Institute carries out financial activities authorized by the AIF, and offers

the following services: acceptance of deposits, asset management, certain custodial functions,

international payment transfers through correspondent banks, and holding salary and pension accounts

of employees of the Holy See and the Vatican City State.

IOR

Annual report 2016

14

The Institute protects its clients’ assets by primarily investing in financial instruments characterized

as very low risk (e.g. government bonds, bonds issued by institutions and international organizations,

as well as deposits in the interbank market).

Credit activity is residual and strictly subject to constraints of the internal policies as established

by the Board of Superintendence.

The IOR does not issue, underwrite or place securities.

Accounts opened at the IOR by authorized customers meet the requirements of the legislation on

preventing and combating money-laundering and the financing of terrorism in force in the Vatican

City State.

Customers are provided with services in IOR offices located in the Vatican City State. The IOR

has no other locations.

3. CORPORATE GOVERNANCE

The IOR’s governance structure is defined in its current Statutes. It consists of five bodies: Commission

of Cardinals, Prelate, Board of Superintendence, Directorate and the Revisori.

The Commission of Cardinals oversees the Institute’s adherence to its Statute. It appoints and removes

members of the Board of Superintendence.

Furthermore:

– It deliberates, after considering the financial statements and taking into account IOR’s own financing

needs, the distribution of profits;

– It proposes to the High Authority changes to the Statute;

– It deliberates the compensation due to members of the Board of Superintendence;

– It approves the appointment and removal of the Director General and of the Vice-Director made

by the Board of Superintendence;

– Resolution of any issues concerning the members of the Board of Superintendence and the Directorate.

IOR

Annual report 2016

Members of the Commission of Cardinals are appointed for a five year term, and can be reappointed.

The current members are:

Cardinal Josip Bozanic Archbishop of Zagabria

Cardinal Santos Abril y Castello President

Archpriest of the Papal Basilica of St Mary Major

Cardinal Christoph Schönborn Archbishop of Vienna

Cardinal Pietro Parolin Secretary of State Cardinal Thomas Christopher Collins

Archbishop of Toronto

Cardinal Jean-Louis Tauran President of the Pontifical Council

for Interreligious Dialoue

15

IOR

Annual report 2016

16

The Prelate is appointed by the Commission of Cardinals. The Prelate:

– Oversees the activities of the Institute and may have access to its acts and documents;

– Participates, as Secretary, in meetings of the Commission of Cardinals, drafting the minutes

of the meeting;

– Attends the meetings of the Board of Superintendence;

– Submits his comments to the Commission of Cardinals, notifying the Board of Superintendence.

Msgr. Battista Mario Salvatore Ricca was appointed as the Prelate of

the Institute in June 2013.

The Board of Superintendence is responsible for the administration and management of the Institute,

as well as the oversight and supervision of its financial, economic and operational activities.

In particular, the Board has the task of:

– Formulating general policy guidelines and basic strategies for the activities of the Institute in

line with its mission;

– Defining the criteria for the implementation of annual programs and objectives of the Directorate,

and approving its proposals;

– Verifying the economic-financial activities of the Institute;

– Monitoring compliance with established programs and objectives, with regard to investments

and other activities;

– Defining the most appropriate financial structure for the Institute, proposing the ways to improve

it, and in general, the best means to increase its assets and activities in the context of correct

adherence to economic-financial rules and in full compliance with the overall mission of

the Institute;

– Proposing to the Commission of Cardinals changes to the Statutes as long as they are unanimously

approved by the Board of Superintendence;

– Arranging for the issuance of the Institute’s Regulations, which are required to provide a detailed

description of the powers and competencies of the Board and of the Directorate;

– Delegating signing power in the name of the Institute to the Director General and, at their request,

the Vice-Director, Managers and Officers, in the manner prescribed in the Regulations;

– Approving the Financial Statements prepared by the Directorate.

The members of the Board of Superintendence are nominated by the Commission of Cardinals and

serve for a five year term, and can be reappointed. The Board consists of 7 members.

IOR

Annual report 2016

Jean-Baptiste de Franssu Mary Ann Glendon

President

Michael Hintze

Mauricio Larrain

Georg Freiherr von Boeselager

(since December 2016)

Scott C. Malpass

(since December 2016)

Javier Martin Romano

(since December 2016)

17

IOR

Annual report 2016

18

The Board of Superintendence fully performed its duties as defined by law and applicable procedures.

It continued to advise and supervise the Directorate in rolling out the agreed reform plan

and provided support for strategically important issues relating to the future development of the

IOR.

In December 2016, 3 new members were appointed to the Board following notably the resignations

of Dr. Carlo Salvatori and Dr. Clemens Boersig. The Board wishes to express its gratitude to

Carlo Salvatori and Clemens Boersig for all the help and counsel they provided to the IOR during

their tenure. The 3 new members, formally appointed on December 15, 2016, are Georg Freiherr

von Boeselager, Scott Malpass and Javier Marin Romano.

In 2016, the Board of Superintendence convened for six meetings and dealt with the strategic and

operating development of the IOR. All members participated in the meetings of the Board of Superintendence

and the committees to which they belong to for the year under review.

The Board continued its work on strengthening IOR standards of corporate governance.The meetings

of the Board of Superintendence continued to represent an open exchange of information and

ideas to find the appropriate resolutions to meet the needs of this unique institution. During these

meetings, the Board benefitted from each member’s specific expertise in various subject matters, and

the Board also held regular executive sessions to discuss specific topics in-depth.

Once approved, the minutes of all Board meetings were shared with the Revisori, the Directorate,

the Prelate and the Commission of Cardinals. During the year, the Board passed resolutions on a

number of matters after careful analysis and consultation, and in close coordination with the Directorate

and the Commission of Cardinals, for which the Board’s consent was mandatory.

In 2015, the Board created two Board committees to strengthen the Governance of the Institute

and the Board’s work, although such committees were not yet provided for by the Statute. An Audit

& Risk and HR & Remuneration committees were first established. In 2016, the Board created

a Past Abuses Committee to help and support the Board in its work of understanding and concluding

the investigation of legacy issues to which IOR was exposed. The Committee completed

its work at the end of January 2017, which included a thorough review of all cases and issued a detailed

set of recommended legal actions. The results of this work has been filed with Vatican Regulator

and Vatican Judicial Authorities.

Minutes were drafted for each committee meeting and distributed to all Board members, along with

a specific report presented by the respective presidents of those committees at each Board meeting

and an annual report at year end.

a) Members of the Human Resources and Remuneration Committee

Mary Ann Glendon – Chair

Carlo Salvatori (until May 2016)

Jean-Baptiste de Franssu (ex officio)

Mauricio Larrain

In attendance: Mario Busso, President of Revisori

b) Members of the Audit and Risk Committee

Sir Michael Hintze – Chair

Leslie Ferrar (non-board member)

Clemens Boersig (until May 2016)

Jean-Baptiste de Franssu (ex officio)

Wiet Pot (non-board member)

In attendance: Mario Busso, President of Revisori

IOR

Annual report 2016

19

c) Members of the Past Abuse Committee (June 2016 – January 2017)

Jean-Baptiste de Franssu – Chair

Sir Michael Hintze

In attendance: Giovanni Barbara, Member of Revisori

A focus was made in 2016 on the development of appropriate control functions, reinforcing their

independence and ensuring that activities and controls were properly carried out. Today, they are

comprised of:

– Internal Audit

– Risk management and Compliance

In accordance with law no. XVIII/2013 (see art. 27 et seq.) and best international practices, the Internal

Audit function reports to the Board with a dotted line to the Directorate.

In terms of second-level controls, Risk management and Compliance department is directly responsible,

among other things, for the AML/CFT (Anti Money Laundering/Combating the Financing

of Terrorism) activities.

The Revisori and the External Auditors have regularly and thoroughly carried out their activities during

2016, as expected.

IOR

Annual report 2016

The Directorate is responsible for all operational activities of the Institute and is accountable to the

Board of Superintendence.

The Directorate is appointed by the Board of Superintendence and approved by the Commission

of Cardinals and consists of:

The Revisori must:

– Verify at least quarterly, the administrative and accounting review of the Institute’s books and

records;

– If requested by the Board of Superintendence, the Revisori may conduct internal audits or other

inspections;

– Review the financial statements including the report of the Directorate and supporting documents,

provide written comments to the Board of Superintendence and present their observations

to the attention of the Directorate and the Prelate.

The Revisori consists of three members, appointed by the Board of Superintendence for a maximum

period of three years. They can be reappointed.

Current members are:

– Mario M. Busso, President of the Revisori

– Giovanni Barbara

– Luca Del Pico

Giulio Mattietti

“Aggiunto al Direttore”

with delegated functions

Gian Franco Mammì

Director General

20

IOR

Annual report 2016

21

4. IOR ORGANIZATION CHART

5. REGULATORY FRAMEWORK AND TAX REQUIREMENTS

Regulatory framework

The Institute is subject to the laws and regulations of the Holy See and Vatican City State.

The Vatican legal framework recognizes the Canon Law as the primary source of legislation and

the primary criterion for its interpretation. Furthermore, there are six organic laws and other ordinary

laws specific to the Vatican City State. For matters not covered by Vatican laws, laws and

other regulations issued by the Italian Republic are observed as supplementary, subject to prior approval

by the competent Vatican authority.They are adopted on the condition that they do not conflict

with the doctrine of divine law, the general principles of Canon Law or the provisions of the

Lateran Pact and subsequent Agreements, and provided that they are applicable to the state of affairs

existing in Vatican City (See law No LXXI on the source of law, promulgated by Pope Benedict

XVI on 1 October 2008).

According to article 1.4 of Law no. LXXI on the sources of law, the legal framework must also conform

to the general norms of international law, and to those arising from treaties and other agreements

to which the Holy See is part of.

The Institute is subject to Law no. XVIII of 8 October 2013 that covers norms of transparency,

supervision, and financial intelligence and, as an entity that carries out financial activities on a professional

basis in Vatican City State, it is also subject to Regulation No. 1 “Prudential Supervision

of Entities carrying out financial activities on a professional basis” issued by AIF and enacted on

13 January 2015.

The Regulation No. 1, establishing a clear system of authorization, stipulates the criteria for the organization

and management of entities and mechanisms of internal control.

IOR

Annual report 2016

DIPARTIMENTO

BILANCIO

DIPARTIMENTO

IT E SICUREZZA

DIPARTIMENTO

OPERATIONS

DIPARTIMENTO

FINANZA

DIPARTIMENTO

GESTIONI

PATRIMONIALI

DIPARTIMENTO

RAPPORTI CON

LA CLIENTELA

COMMISSIONE CARDINALIZIA

PRELATO

RISK MANAGEMENT

E COMPLIANCE

SEGRETERIA

DI PRESIDENZA

LEGALE

INTERNAL AUDIT

RISK MANAGEMENT

COMPLIANCE ED

ANTIRICICLAGGIO

CONSIGLIO DI SOVRINTENDENZA

DIREZIONE SEGRETERIA

DI DIREZIONE

SEGRETERIA

AMMINISTRATIVA

ORGANIZZAZIONE E

RISORSE UMANE

DIPENDENZA FUNZIONALE DIPENDENZA GERARCHICA DIPENDENZA AMMINISTRATIVA

On 15 December 2016, the AIF promulgated the “Circular relating to the preparation of the annual

financial statements and the consolidated financial statements of entities carrying out financial

activities on a professional basis”. These financial statements have been prepared in accordance

with the aforementioned Circular.

Tax requirements

On 15 October 2016 the “Agreement between the Government of the Italian Republic and the Holy

See in tax matters” became effective. The Agreement had also a two-fold impact on the Institute’s

activities. In fact, the agreement provides for clients resident in Italy for tax purposes, on one hand,

the regularization of the client positions in the prior years from 2010 to 2015 and, on the other

hand, henceforth, that clients fulfill their tax debts through a Fiscal Representative chosen by the

Institute. Concerning previous years it has been provided by a specific implementing act of the Secretary

of State that the IOR assist its clients in compiling the instance with reference to the data

regarding the investments held at the Institute and the calculation of taxes due, in addition to all

the related administrative tasks. For the current and future period, the IOR must provide the calculations

and withhold taxes to customers which will be paid to the Italian Government via an Italian

tax representative.

This required significant efforts to be made prior to the affectiveness of the agreement and in the

following months. A specifictask force was established at the Institute to provide assistance to clients

with the calculation of the amounts due and related administrative activities.

Effective 2015, the IOR is subject also to the Foreign Account Tax Compliance Act (FATCA), a

United States federal law that requires U.S. persons, including individuals who live outside the

United States, to report their financial accounts held outside of the United States to the U.S. Internal

Revenue Service (IRS).

FATCA also requires foreign financial institutions to report to the IRS the accounts of their U.S.

clients. In this context, the Holy See has reached an Intergovernmental agreement (IGA) with the

United States signed in June 2015. Under the terms of the IGA, the Holy See is a jurisdiction treated

by the US Authorities as if the IGA was effective as of 30 November 2014, and the IOR has been

assigned an identification code (GIIN) by the IRS. The IOR fully complies with the terms of the

IGA.

6. PROPOSAL OF DISTRIBUTION OF THE NET PROFIT FOR THE YEAR

For the net profit for the year ended 31 December 2016 amounting to EUR 36.0m, the Board of

Superintendence intends to propose to the Commission of Cardinals, that the profits be distributed

in full without making any provision to the Reserves, also considering the adequacy of capital

(for further details see Part 6 – paragraph 6.2.2 “Capital adequacy”).

22

IOR

Annual report 2016

CHAPTER 2

OPERATIONAL INFORMATION

1. 2016 BUSINESS REVIEW

Macroeconomic environment

Below is an overview of the macroeconomic environment that characterized 2016, with particular

reference to those markets and events that had the strongest influence on the performance of the

Institute’s portfolio.

In 2016, financial market trends were characterized by the sharp increase in uncertainty and there

were also several factors that increased risk aversion. In the first few weeks of the year, fears of a slowdown

in advanced economies intensified, first and foremost in the US economy, in addition to fears

of a contraction in the Chinese economy.The expectations of a new economic crisis that could have

a domino effect to all the international markets therefore increased. Concerns over China also affected

the market for raw materials and oil prices dropped to the lowest level of the year.

This turbulent start was followed by a mild recovery that lasted until the major electoral appointments

of the year, the British Brexit referendum, the US elections and the Italian constitutional referendum.

Although the outcomes were not what financial operators had hoped for, the markets

proved to be unexpectedly resilient. In the UK, the outcome of the referendum to decide on whether

or not to remain in the European Union resulted in a sharp devaluation of the Pound and led to

the adoption of expansionary monetary measures. In the United States, the “shock” of Trump’s victory

was instead short-lived. His victory was viewed as a turning point attributed to announcements

of implementation of fiscal stimulus measures, tax cuts and a corporate law reform, fuelling expectations

of higher inflation. In Italy, while the victory of the “No” vote on the constitutional reform

last December led to Prime Minister Renzi’s resignation, it did not result in the feared meltdown

on Italian government bonds.

At the macroeconomic level, 2016 was a year of modest growth for both Europe and the United

States, with contrasting trends during the year. US economic growth was lower than expected in

the first half. Indicators improved half way through the year, signalling the possibility of an increase

in manufacturing activity towards the end of the year. However, 2016 ended with a slowdown in

economic growth at 1.9% in the fourth quarter, although employment rates and incomes continued

to grow. In the Eurozone, there were conflicting economic indicators. Quarterly GDP growth

slowed during the April – June period, but the annual change remained sufficient to promote a grad- 23

IOR

Annual report 2016

Gian Franco Mammì

Director General

Istituto per le Opere di Religione

ual improvement in the labor market with a steady absorption of the unemployment rate, which

still remains high. Inflation gradually increased towards the end of the year due to the rise in energy

prices.

Central Bank Monetary Policies continued to be expansionary in many countries over the year. In

March, the ECB cut interest rates, introduced new monetary stimulus measures extending, at least

until the end of 2017, the government bond purchase program in order to jump start economic

growth. By contrast, in the wake of the economic improvement, the US Federal Reserve decided

to raise interest rates by 25 basis points in December, widely expected by the market.

The bond markets reacted positively for most of the year. The ECB’s measures, combined with low

inflation, have lowered yields on government securities in all sectors, with the yield on German tenyear

bonds becoming negative. Italian government securities also benefited from the ECB’s purchase

program that helped keepTreasury bond yields low (10-yearTreasury bond yield was 1.25% in midyear,

after having peaked at 1.7% in February) and limited the spread on German bond yields during

turbulent market phases.Towards the end of the year, US, Japanese and EuropeanTreasury bond

yields rose significantly, resulting in a significant reversal of the bond curve as a result of a change

in the expectations of rising interest rates and expansionary fiscal policies aimed to counter weak

economic growth. Bond rates remained very low but with the risk of an increase.

During 2016 the stock market was severely affected by political events, with European stocks showing

lower yield trends compared to the US given the concerns about a possible disruption in the European

political scenario, also as a result of the UK referendum.The first nine months of 2016 were

characterized by pronounced volatility and heightened risk aversion among investors in the main

international markets, particularly, in the Eurozone and Asia. In June, the unexpected victory of the

“Leave” campaign in the Brexit referendum brought about a sharp downward adjustment in share

prices and a new increase in investors’ risk aversion (share prices in Italy experienced a sharp decline

with a mid-year high of -25%, with twice that on the Italian banking sector index) before recovering

towards the end of the year thanks to the improvement in the US economy, the continued flow

of liquidity provided by monetary policies and the expectations of procyclical fiscal policies.

Currencies were at the forefront of news reports in 2016, particularly in the UK following the outcome

of the referendum: in fact, the Pound immediately fell 10% against the dollar to close the year

at -16%. The Euro declined against the dollar, due to the increasing marked divergence in terms

of monetary policy. Overall, 2016 was another very positive year for the US dollar, against which

the Euro and the Swiss Franc, in addition to the Pound, lost value. Instead, the Japanese Yen held

its ground.

Lastly, with regards to raw materials, we experienced fluctuations in the prices of gold and oil. After

almost two years of decrease in the prior of oil, the major commodity indices seems to have stabilized,

going from 26 dollars per barrel in January 2016 to 50 dollars towards the end of year, in

part to the agreement reached by OPEC. Gold, as the main safe haven asset in times of high risk

aversion, peaked in the first half of 2016, having risen from its lowest price at 1061$/oz in December

up to 1370$/oz in July. In the second half of the year, except for the short-lived surge that followed

the election of Donald Trump, gold prices suffered to the point of reaching its lowest price

in 10 months: 1,122.35$/oz, mainly because of the FED’s announcement of an increase in interest

rates and the expectation of another three increases in 2017.

Composition of the Client base

At the end of 2016, the IOR had 14,960 clients (2015: 14,801), of which the vast majority, measured

by assets entrusted to the Institute, were legal persons under Canon Law.The IOR’s customers

have a common characteristic, which is that they are part of and serve the Catholic Church (seeclient

definition in Chapter 1). 24

IOR

Annual report 2016

IOR

Annual report 2016

25

Measured by assets entrusted, the most important group of clients, was religious orders. They accounted

for more than half of our client base in 2016 (54%), followed by Roman Curia departments,

Holy See Offices and nunciatures (11%), entities of Canon Law (9%), cardinals, bishops

and clergy (8%), episcopal conferences, dioceses and parishes (8%), with the remainder split between

various others, such as Vatican employees and pensioners and Canon Law foundations.

In addition to depositing funds with us, we manage our clients’ portfolios of assets on their behalf

or act as custodians. As of 31 December 2016, the net value of assets held in managed portfolios

was EUR 3.1bn (2015: EUR 3.2bn), the net value of assets held in non-managed portfolios was

EUR 554.8m (2015: EUR 646.2m) and the value ofcustomer deposits was EUR 2.0bn (2015: EUR

1.9bn), resulting in EUR 5.7bn in total client assets (2015: EUR 5.8bn).

(in thousand Euro)

2016 2015

In Balance Off Balance Total In Balance Off Balance Total

Sheet Sheet Sheet Sheet

Customer deposits

(including Legates) 2,028,973 2,028,973 1,946,854 1,946,854

Assets under Custody 554,763 554,763 646,161 646,161

Assets under Management 410,563 * 2,700,366 3,110,929 424,815 2,760,870 3,185,685

Total 2,439,536 3,255,129 5,694,665 2,371,669 3,407,031 5,778,700

*Deposits of Assets Management are net of commissions collected in the first days of 2017.

Assets under Custody mainly include client-owned securities held at the IOR for custodial purposes.

The clients make all investment decisions and the IOR has no discretionary power to manage these

assets, provided that such decisions are in accordance with the role and mission of the Institute. For

the purpose of table above, securities, gold and precious metals under custody are stated at market

values.

Assets under Management consist mainly of client-owned securities held at the IOR for management

purposes. Investment decisions are made by the IOR on the basis of portfolio management

mandates signed with its clients. For the purpose of table above, securities under management are

stated at market values.

Income Statement

In 2016, IOR’s Net profit was EUR 36.0m (2015: EUR 16.1m).Theincreasefrom 2015 was mainly

due to improved results from Net Income for trading activities, to the remeasurement of a provision

for tax remediation to foreign countries recognized in 2015 and to the decrease in Administrative

expenses.The results were partially offset by the decrease in Interest Margin and Net fee and

commission income.

A brief overview of the main components of the Income Statement is presented below.

The most significant source of revenues is the profit derived from Treasury activities on proprietary

portfolios.

The most important component was derived from bond yield which contributed for EUR 39.6 million

(interests EUR 38,0 million plus trading results EUR 1.6 milion).

Interest Margin amounting to EUR 36.7m decreased by 16% compared to EUR 43.6m in 2015.

This was mainly affected by the decline in the yield on investments in securities and bank deposits

and a decline in interest paid to customers, although the average amounts of capital invested re-

IOR

Annual report 2016

26

mained unchanged at EUR 2.9bn (2015: EUR 2.9bn); The average rate on customer deposits declined

to 0.11% in 2016 from 0.22% in 2015, while the average yield on investments in securities

and bank deposits declined to 1.35% in 2016 from 1.64% in 2015. Accordingly, the spread

between the average rate received on assets and the average rate paid on liabilities decreased to 1.24%

from 1.42%.This was mainly due to the expiration of securities in 2016 purchased in previous years

with a nominal interest rate higher than those currently available on market.

Net Income for trading activities recognised a net loss of EUR 9.0m compared to a net loss of EUR

15.4m in 2015. The result was mainly affected by the decrease in UCI unit investment compared

to 2015, amounting to EUR -12.8 milion. The improvement in the results was mainly due to the

positive performance of the bonds held in the proprietary portfolio in 2016, compared to 2015,

to market trends during the year.

More specifically, debt securities recognised a positive total net profit, including gains and losses

from trading and gains and losses from valuation, amounting to EUR 1.6m in 2016 compared to

a loss of EUR 17.1m in 2015.

Equity securities recorded a profit of EUR 94,000 in 2016, versus a loss of EUR 307,000 in 2015,

while FX activity contributed for EUR 2.0 million versus EUR 1.9 million in 2015.

The value of UCI unit investment decreased by 2015 due to the write-down of an investment fund

held in the portfolio in addition to other losses for a total of EUR 12.8 million in 2016 versus EUR

149.000 in 2015.

Dividends increased by 7.8% to EUR 2.1m from EUR 2.0m in 2015.

Net Fee and Commission income decreased 15.9% to EUR 12.8m in 2016 from EUR 15.2m in

2015. Fee and Commission Income decreased 10.6% to EUR 15.8m in 2016, from EUR 17.7m

in 2015, while Fee and Commission Expense rose to EUR 3.0m in 2016 from EUR 2.5m in 2015

(+22.1%).

The most important component of the Fee and Commission Income was commissions from Asset

Management services, which decreased 8.7% to EUR 12.5m in 2016 from EUR 13.7m in 2015.

This was mainly due to the shift of some customers to asset management lines, mainly composed

by bond securities, with lower commissions than lines composed mainly by equity securities, that

the same clients owned before.

The increase in Fee and Commission Expense was mainly due to the fees paid for bank deposits

(EUR 571,000 in 2016), paid for the first time in 2016, and to the increase in commission paid

for custody and administration of securities, amounting to EUR 1.6m in 2016 from EUR 0.9m

in 2015. This is partially offset by the decrease in commission paid for trading in financial instruments,

which decreased to EUR 83,000 in 2016, from EUR 648,000 in 2015, due to the fact that,

starting from 2016, clients directly pay commissions on securities transactions whereas previously,

they were paid by the Institute and collected later.

Administrative Expenses were EUR 19.1m in 2016 (2015: EUR 23.4m). This includes Staff Expenses

of EUR 10.2m in 2016, in reduction with the prior year amount (2015: EUR 11.3m, or –

9.1%). As of December 31, 2016, the IOR had a total of 102 personnel (2015: 109). During the

year, six employees retired and one resigned.

Administrative expenses also include expenses for professional services, which decreased from

EUR 7.6m in 2015 to EUR 4.0m in 2016.This was due to lower extraordinary costs incurred during

the year from the completion of certain projects.

IOR

Annual report 2016

27

Other administrative expenses slightly increased by 7.2% to EUR 4.9m in 2016 from EUR 4.6m

in 2015 due to higher costs incurred for maintenance.

Net provisions to risks and charges in 2016 amounted to a profit of EUR 13.0m (2015: loss of

EUR 16.5m) due to the reestimation of a tax provision for exposure in foreign countries recorded

in 2015.

Other Operating Income (Expense) recognised income of EUR 7,000 (2015: income of EUR

10.5m); the difference, compaired to the previous year, is mainly due to EUR 13.6m of extraordinary

income recorded in 2015 related to the closing of an issue from prior years.

Balance Sheet

As of 31 December 2016, total assets on the IOR’s balance sheet was EUR 3.3bn (2015: EUR

3.2bn), with equity of EUR 672.6m (2015: EUR 670.3m).

On the Liabilities side, Due to customers is the most significant line item, representing 92.4% of

total liabilities. The balance slightly increased from the prior year, amounting to EUR 2.4bn

(+3.3%). Customer deposits increased by EUR 75.5m, while asset management liquidity decreased

by EUR 14.3m.

Our clients expect a conservative approach in financial management by the IOR, with investments

in liquid securities and high quality credit risk. Investments in the stock market and similar financial

instruments are relatively limited and based on companies with strong fundamentals which generally

tend to pay high dividends.

No funding activities are carried out on the interbank market and IOR does not issue debt securities.

As previously reported in Chapter 1, credit activity is residual and strictly subject to constraints of

the internal policies as established by the Board of Superintendence.

The asset side of the balance sheet mainly reflects bank deposits and securities, and less than 3%

of total assets is held in UCI units and equities.

Bank Deposits totaled EUR 643.2m at the end of 2016 (2015: EUR 644.1m). These mainly consisted

of EUR 457.6m in deposits on demand (2015: EUR 265.4m), and EUR 108.5m in term

deposits in the interbank lending market (2015: EUR 292.5m). The remaining part, EUR 77.1m

(2015: EUR 60.7) concerned term deposits with APSA.

The value of IOR Securities (debt securities, equity securities and investment funds) was EUR 2.5bn

in 2016 (2015: EUR 2.3bn). Bonds, at EUR 2.4bn, were the most significant investments, representing

96.3% of the securities held as of 31 December 2016, while equities accounted for 2.4%,

and investment funds for 1.3%. As previously explained, the volume of the securities in the portfolio

slightly increased compared to 2015, while the portfolio composition remained unchanged.

Profitability ratios

The table below highlights the main economical, financial and productivity ratios:

Profitability ratios (%) 2016 2015

ROE (Returns on Equity) 5.66% 2.47%

ROA (Returns on Assets) 1.10% 0.50%

Operating costs / Earnings margin 15.52% 66.05%

Interest margin / Earnings margin 83.15% 96.03%

Net fee and commission income / Earnings margin 29.05% 33.51%

Interest margin / Total Assets 1.12% 1.36%

Earnings margin / Total Assets 1.35% 1.42%

The ratios ROE and ROA recorded an increase compared with the previous year due to the increase

in Net profit.

The profitability, explained from the ratio “interest margin / total assets”, amounted in 2016 to

1.12% against 1.36% recorded in 2015, due to the reduction of interest margin; the ratio “earnings

margin / total assets” recorded almost a result in line with the previous year (1.35% in 2016,

1.42% in 2015).

These two ratios showed that the Institute ability to create income slightly decreased, but the negative

effects were balanced by the decrease of operating costs, showing good flexibility in reacting

promptly to market changes.

Other aspects

The IOR does not issue securities, neither underwrite or place securities; it protects its client assets

by primarily investing in financial instruments characterized as very low risk (e.g. government

bonds, bonds issued by institutions and international organizations, as well as deposits in the interbank

market).

The IOR has no branches and provide services only at the IOR office located in the Vatican City

State.

The Institute owns 100% of the real estate company SGIR S.r.l., with registered office in Italy. The

Institute has a long-term zero-interest loan to its subsidiary SGIR S.r.l., amounting to EUR 3.3m.

During 2015, the Institute signed a loan agreement for the use of 4 real estate properties at no cost

with its subsidiary SGRI S.r.l. During 2016, SGIR S.r.l. did not earn rental income on these properties.

2. FORECAST FOR 2017

In the first months of 2017, the Institute’s activity was in line with the Strategic Plan approved by

the Board of Superintendence in January 2017.The main objective is to improve the quality of services

offered to clients. The forecast for 2017 is a stable base of customer deposits, a result of a balance

between the outflows due to the tax agreements signed between the Holy See and other countries

and inflows due to the increased quality of services offered. By the end of 2018, the results of

this work should be apparent.

The effort, already undertaken in recent years, to comply with Holy See laws and regulations and

international best practice will continue to be implemented.The same will apply with international

tax matters. 28

IOR

Annual report 2016

The issues of transparency and reputation will obviously be the core in this process of growth; many

steps and activities have been taken from 2013 to make the Institute more transparent and aligned

with international best practices.

The IOR will continue to operate in accordance with his Mission that is to serve the Holy Father

with prudence, in His mission as the Universal Pastor, through the provision of dedicated financial

advisory, in complete compliance with Vatican and international laws in force and with what

the Holy Father said “the main goal of the IOR cannot be to have the maximum possible gain, but

should be goals that are compatible with the norms of morality, consistent efficiency and practices

respecting the specificity of its nature and exemplarity in its mode of operation”.

29

IOR

Annual report 2016

FINANCIAL STATEMENTS

IOR

Annual report 2016

33

BALANCE SHEET

IOR financial statements for 2016 are prepared in accordance with the Circular concerning the annual

financial statements and the consolidated financial statements of entities carrying out financial

activities on a professional basis, issued by Authority of Financial Information on 15 December

2016.

The 2015 figures have been reclassified according to the provisions of the Circular above mentioned.

(in Euro)

ASSETS 2016 2015

10. Cash and cash equivalents 50,850,340 114,737,182

20. Financial assets held for trading 1,918,104,346 1,667,965,933

40. Financial assets available for sale 6,664,406 15,167,415

50. Financial assets held to maturity 558,955,610 614,818,290

60. Due from banks 643,229,012 644,089,443

70. Due from customers 29,152,785 86,233,851

100. Investment in subsidiaries 15,834,950 15,834,950

110. Tangible assets 3,095,565 2,981,724

120. Intangible assets 1,043,850 874,809

150. Other assets 41,958,806 41,556,606

Total Assets 3,268,889,670 3,204,260,203

LIABILITIES AND EQUITY 2016 2015

10. Due to banks 10,597,312

20. Due to customers 2,398,924,457 2,323,402,903

100. Legates 47,074,644 48,266,303

110. Other liabilities 18,709,825 20,086,868

120. Staff severance fund 6,992,585 6,788,489

130. Provision for risks and charges 124,588,179 124,838,475

(a) Provisions for pensions and similar obligations 121,088,179 108,338,475

(b) Other provisions 3,500,000 16,500,000

140. Valuation reserves (45,534,851) (27,981,254)

160. Reserves 382,134,172 382,134,172

(a) Unavailable reserves 100,000,000 100,000,000

(b) Available reserves 282,134,172 282,134,172

170. Capital 300,000,000 300,000,000

180. Net profit for the year 36,000,659 16,126,935

Total Liabilities and Equity 3,268,889,670 3,204,260,203

34

IOR

Annual report 2016

INCOME STATEMENT

(in Euro)

INCOME STATEMENT 2016 2015

10. Interest and similar income 39,831,730 48,640,984

20. Interest and similar expense (3,168,836) (5,002,810)

30. Interest margin 36,662,894 43,638,174

40. Fee and commission income 15,836,850 17,709,979

50. Fee and commission expense (3,029,222) (2,481,584)

60. Net fee and commission income 12,807,628 15,228,394

70. Dividends and similar income 2,107,013 1,954,367

80. Net income for trading activities (8,982,924) (15,377,567)

100. Profit (loss) on disposal or repurchase of: 1,499,109

(b) Financial assets available for sale 1,499,109

120. Intermediation margin 44,093,720 45,443,368

130. Net losses/reversal on impairment: (1,331,864) 197,034

(a) Receivables (1,045,306) 352,909

(b) Financial assets available for sale (148,314)

(d) Other financial operations (138,244) (155,875)

140. Net income from financial operations 42,761,856 45,640,402

150. Administrative expenses: (19,085,562) (23,427,846)

(a) Staff expenses (10,244,959) (11,268,224)

(b) Professional services expenses (3,961,573) (7,607,374)

(c) Other administrative expenses (4,879,030) (4,552,248)

160. Net provisions to risks and charges 13,000,000 (16,500,000)

170. Net value adjustments to/recoveries on tangible assets (82,789) (63,868)

180. Net value adjustments to/recoveries on intangible assets (682,777) (511,793)

190. Other operating income (expense) 7,287 10,489,260

200. Operating costs (6,843,841) (30,014,247)

220. Net result of fair value valuation of tangible and intangible assets 82,644 500,780

250. Profit (loss) from current operations before taxes 36,000,659 16,126,935

270. Profit (loss) from current operations after taxes 36,000,659 16,126,935

290. Profit (loss) for the year 36,000,659 16,126,935

IOR

Annual report 2016

35

STATEMENT OF COMPREHENSIVE INCOME

(in Euro)

2016 2015

10. Profit (loss) for the year 36,000,659 16,126,935

Items that will not be reclassified to Income Statement

40. Defined benefit plans (13,275,014) 8,880,551

Items that are or may be reclassified to Income Statement

100. Financial assets available for sale (4,278,583) 4,777,470

130. Total other income items (17,553,597) 13,658,021

Comprehensive income (item 10 + item 130) 18,447,062 29,784,956

STATEMENT OF CHANGES IN EQUITY

(in Euro)

2016 Allocation of Changes during the year

previous year profit

Total net equity Changes in Total net equity Reserves Dividends Changes Extra Comprehensive Net

at 31.12.2015 opening at 01.01.2016 and other in reserves dividend income Equity at

balances allocations distribution 2016 31.12.2016

Capital 300,000,000 300,000,000 300,000,000

Reserves

(a) unavailable 100,000,000 100,000,000 100,000,000

(b) available 282,134,172 282,134,172 282,134,172

(c) other

Valuation

reserves (27,981,254) (27,981,254) (17,553,597) (45,534,851)

Net profit

(loss) for

the year 16,126,935 16,126,935 (16,126,935) 36,000,659 36,000,659

Net Equity 670,279,853 670,279,853 (16,126,935) 18,447,061 672,599,980

(in Euro)

2015 Allocation of Changes during the year

previous year profit

Total net equity Changes in Total net equity Reserves Dividends Changes Extra Comprehensive Net

at 31.12.2014 opening at 01.01.2015 and other in reserves dividend income Equity at

balances allocations distribution 2015 31.12.2015

Capital 300,000,000 300,000,000 300,000,000

Reserves

(a) unavailable 100,000,000 100,000,000 100,000,000

(b) available 267,300,717 267,300,717 14,833,455 282,134,172

(c) other

Valuation

reserves (41,639,275) (41,639,275) 13,658,021 (27,981,254)

Net profit (loss)

for the year 69,333,455 69,333,455 (14,833,455) (54,500,000) 16,126,935 16,126,935

Net Equity 694,994,898 694,994,898 (54,500,000) 29,784,954 670,279,853

36

IOR

Annual report 2016

CASH FLOW STATEMENT

(in Euro)

2016 2015

A. Operating activities

1. Management 42,833,712 48,037,261

Interest income 48,639,880 55,060,588

Interest expense (3,168,341) (7,659,915)

Dividends and similar income 2,107,013 1,954,367

Net commissions 12,807,628 15,228,394

Realised profit (loss) from trading activities 2,024,715 (6,521,066)

Staff expenses (10,566,173) (10,043,861)

Other administrative expenses (8,840,603) (13,323,635)

Other income (expense) (170,407) 13,342,389

2. Cash generated by/used in financial assets (206,618,819) 68,576,005

Financial assets held for trading (266,429,528) 41,765,424

Financial assets available for sale 5,575,219

Due from banks: on demand (192,197,353) 17,854,851

Due from banks: other receivables 192,249,112 (48,714,530)

Due from customers 54,408,236 61,305,128

Other assets (224,505) (3,634,868)

3. Cash generated by/used in financial liabilities 62,216,802 13,182,507

Due to banks: on demand (10,591,428) 10,581,312

Due to banks: other payables

Due from customers 75,515,176 12,469,195

Outstanding securities

Legates (1,191,659)

Financial liabilities held for trading

Financial liabilities carried at fair value

Other liabilities (1,515,287) (9,868,000)

Cash generated by/used in operating activities (101,568,305) 129,795,773

B. Investing activities

1. Cash generated by: 53,250,000 64,986,522

Disposals of investments in subsidiaries

Dividends received on investments in subsidiaries

Disposal/reimbursement of financial assets held to maturity 53,250,000 64,986,522

Disposals of tangible assets

Disposals of intangible assets

2. Cash used in: (965,804) (34,206,681)

Purchases of investments in subsidiaries

Purchases of financial assets held to maturity (33,412,000)

Purchases of tangible assets (113,986) (240,681)

Purchases of intangible assets (851,818) (554,000)

Cash generated by/used in investing activities 52,284,196 30,779,841

C. Financing activities

Issues/purchases of capital instrument

Dividend distribution and other purposes (16,126,935) (54,500,000)

Cash generated by/used in financing activities (16,126,935) (54,500,000)

Cash generated/used during the year (65,411,044) 106,075,614

IOR

Annual report 2016

37

Items 2016 2015

Cash and cash equivalents at beginning of the period 114,737,182 16,351,306

Cash generated/used during the year (65,411,044) 106,075,614

Cash and cash equivalents: forex effect 1,524,202 (7,689,738)

Cash and cash equivalents at end of the period 50,850,340 114,737,182

EXPLANATORY NOTES

PART 1. ACCOUNTING POLICIES

1.1 GENERAL INFORMATION

1.1.1 Statement of compliance with accounting standards

The 2016 financial statement have been prepared in accordance with the Circular concerning the

annual financial statements and the consolidated financial statements of entities carrying out financial

activities on a professional basis, issued by Authority of Financial Information on 15 December

2016.

As stated in the Circular, the financial statements must be prepared in accordance with the “International

Accounting Standards – IAS”, the “International Financial Reporting Standards – IFRS”

and related Interpretations (“Interpretations SIC / IFRIC”), as adopted by the Vatican in a special

arrangement to the Monetary Convention between the European Union and the State of the Vatican

City on 17 December 2009.

The 2015 figures have been reclassified according to the provisions of the above mentioned Circular.

1.1.2 Accounting policies

The financial statements consist of the Balance Sheet, the Income Statement, the Statement of Comprehensive

Income, the Cash Flow Statement, the Statement of Changes in Equity and the Explanatory

Notes.

Disclosures under IFRS 7 “Financial Instruments, disclosures” about the nature and extent of risks

have been included in Part V “Information on Risks and Hedging Policies”.

The accounting principles and valuation methods applied in the preparation of these financial statements,

detailed below, are consistent with those of the previous financial year, except for new standards,

new interpretations, or amendments of standards and except for gold, silver, medals and precious

coins evaluation criteria. According to AIF Circular and IAS 2, starting from 1 January 2016,

gold, silver, medals and precious coins are measured at the lower of cost and net estimated recoverable

amount, as explained in the Section 1.1.4 “Other Aspects”.

The financial statements of the Institute are prepared in Euro, while the explanatory notes are expressed

in thousand Euro.

For the various items, the 2016 figures and corresponding values for the previous year are provided.

Where necessary, the comparative figures have been adjusted to conform to changes in presentations

in the current year.

The financial statements are prepared in Italian.

The financial statements of the IOR were prepared on a going concern basis in accordance with

IAS 1 “Presentation of Financial Statements”. As of the date of the approval of the financial statements,

there were no material uncertainties and therefore no significant doubt regarding the Institute’s

ability to continue as a going concern in the foreseeable future. 38

IOR

Annual report 2016

The financial statements fairly present the financial position, financial performance and cash

flows of the Institute.

The preparation of the financial statements requires the Directorate to make certain estimates and

assumptions about the future where actual results may differ. Estimates and assumptions affect the

reported amounts of certain assets, liabilities, revenues and expenses in the financial statements. In

addition, changes in assumptions may have a significant impact on the financial statements in the

year in which the assumptions change.

The preparation of the financial statements also requires the Directorate to exercise judgements in

applying the IOR’s accounting policies to estimate the carrying value of assets and liabilities not

readily obtainable from other sources.

The Directorate believes that the underlying assumptions are appropriate and that the IOR’s financial

statements fairly present its financial positions and results. All estimates are based on historical

experience and/or expectations with regard to future events that seem reasonable on the basis

of information known at the time of the estimate. They are also reassessed on a regular basis and

the effects of any variation are immediately reflected in the financial statements.

Those areas involving a higher degree of judgement or complexity, or areas where assumptions and

estimates are significant to the financial statements, are disclosed in Section 1.1.4.1. “Critical accounting

estimates and judgements”.

The financial statements do not reflect a provision for taxes because there is no corporate income

tax in Vatican City State.

The Institute, given the immaterial value of its subsidiary, does not prepare consolidated financial

statements in accordance with the provisions of the Conceptual Framework (QC6 – QC11) of

IAS/IFRS, since the additional information coming from the consolidated financial statements

would be of little relevance for the users of the financial statements.

The Institute provides the additional information required by IFRS 12 “Disclosure of interests in

other entities” in Part 5, Section 5.2.6 “Disclosure of unconsolidated structured entities for accounting

purposes”.

The financial statements of the Institute are prepared by the Directorate and approved by the Board

of Superintendence, which will be submitted to the Commission of Cardinals.

The Commission of Cardinals acknowledges the financial statements and decides on the distribution

of profits, after taking into account the IOR’s own financing needs.

1.1.3 Subsequent events

According the provisions of IAS 10, all events that took place subsequent to 31 December 2016

have been evaluated in the preparation of the 2016 Financial Statements.

1.1.4 Other aspects

Starting from the financial year 2016 IOR applies the provisions arranged by the AIF Circular issued

on 15 December 2016 about gold, silver, medals and precious coins. The Circular provides

that gold, silver, medals and precious coins are normally carried at the lower of cost (see IAS 2, paragraphs

10-18) and net estimated recoverable amount (see IAS 2 paragraphs 6-7). 39

IOR

Annual report 2016

According to IAS 8, the Institute considered the value as at 1 January 2015 (31 December 2014)

as cost of the gold, silver and precious medals and coins, because was not feasible to make a measurement

for the prior years.

As of 31 December 2015, the value of gold was lower than the cost and this involved only a reclassification

of the loss, already recorded in the previous financial year, from the item “Net income

for trading activities” to the item “Other operating income (expense)”; no other economic impacts

were recorded.

The gold, silver, medals and precious coins held by the Institute are classified in the Balance Sheet,

Item 150 Assets – “Other assets”. Gold is mainly deposited with the U.S. Federal Reserve, while

medals and precious coins are kept in the IOR vaults.

1.1.4.1 Critical accounting estimates and judgements

Critical judgements in applying the Institute accounting policies

In the process of applying the accounting policies adopted by IOR, which are described in Section

II, there may be circumstances that lead the Directorate to make judgements that have a significant

impact on the amounts recognized in the financial statements.

Such circumstances and related judgements may be part of the valuation process used for financial

instruments. The Directorate makes critical judgements when deciding the asset category for classification,

determining whether a market is active or not, whether the asset is liquid or illiquid, market

inputs and parameters to be used, when they must be reviewed, and assessing circumstances

where internal parameters are more reliable than market-based ones.

Retirement benefits and other post-employment liabilities are estimated trough an actuarial valuation

performed by an independent expert. Such an evaluation is based on critical judgements because

estimates are made about the likelihood of future events and the actual results could differ

from those estimates.

Estimates that contain elements of uncertainty

The process of applying the IOR’s accounting policies may require the use of key assumptions affecting

the future, and/or other sources of estimation uncertainty as of the balance sheet date, with

a significant risk of causing material adjustments to the carrying amount of assets and liabilities in

the next financial year.

Key assumptions and judgments made in the 2016 Financial Statements relate to the assessment

of illiquid debt securities portfolio held for trading and external investment funds included within

the portfolio held for trading, as disclosed in the section 1.4 “Fair value information”.

Illiquid securities are not quoted in active markets and their fair value is not readily available in the

market.These securities subject estimation uncertainties (Level 3 of fair value hierarchy) amounted

to EUR 23.3m as of 31 December 2016 (2015: EUR 35.9m). These were exclusively comprised

of externally managed investment funds.

With reference to the liabilities related to commitments linked to externally managed investment

funds, they are valued taking into account all available information at the date of preparation of

these financial statements. This assessment is made on the basis of assumptions and the process of

estimation in characterized by elements of uncertainty. By their nature, the estimates and assumptions

used may vary from one period to another and, therefore, it can not be excluded that in subsequent

periods the amounts of such liabilities may differ materially from those currently estimated

as a result of new information and charges in the evaluations made. 40

IOR

Annual report 2016

The IOR has also been working to review and confirm its tax position and that of its clients in countries

where investment relationships exist. This review has identified probable contingencies that

relate to prior years as a result of different interpretations regarding the legal nature of the Institute

and the related applicable tax treatments.

As of 31 December 2016, based on the reviews performed and supported by external legal advisors,

the Institute has estimated a provision of EUR 3.5m, included in the Balance Sheet, item 130

“Provision for risks and charges” line b “Other provisions”. As this represents an estimate based on

critical assumptions, actual results may differ from what is expected when the future event takes

place.

1.1.5 Impact of New Accounting Pronouncements

Accounting standards, amendments and interpretations IFRS effective 1 January 2016

The following accounting standards, amendments and interpretations IFRS were adopted for the

first time by the IOR effective 1 January 2016:

• Amendments to IAS 19 “Defined Benefit Plans: Employee Contributions” (published on 21

November 2013): the amendments relate to the accounting treatment for contributions made

by employees or third parties to a defined benefit plan. The adoption of the amendments had

no impact on the disclosures or the amounts recognized in the Institute’s financial statements.

• Amendments to IFRS 11 “Accounting for acquisitions of interests in joint operations” (published

on 6 May 2014): the amendments provide guidance on how to account for the acquisition

of an interest in a joint operation whose activities constitute a business. The adoption of

the amendments had no impact on the disclosures or the amounts recognized in the Institute’s

financial statements.

• Amendments to IAS 16 and to IAS 38 “Clarification of acceptable methods of depreciation and

amortisation” (published on 12 May 2014):The amendments prohibit the use of revenue-based

depreciation; the revenue generated by an activity that includes the use of the asset to be depreciated

generally reflects factors other than just the consumption of economic benefits of the

asset, which is a requirement for depreciation. The adoption of the amendments had no impact

on the disclosures or the amounts recognized in the Institute’s financial statements.

• Amendment to IAS 1 “Disclosure Initiative” (published on 18 December 2014): the purpose

of the amendment is to provide clarification on disclosure items that may be perceived as presenting

impediments to a clear and intelligible preparation of financial statements. The adoption

of the amendments had no impact on the disclosures or the amounts recognized in the Institute’s

financial statements.

• Amendment to IAS 27 Equity Method in Separate Financial Statements (published on 12 August

2014): the amendment introduces the option to use the equity method in the separate financial

statements of an entity for the valuation of investments in subsidiaries, jointly controlled

entities and associated companies.The adoption of the amendments had no impact on the disclosures

or the amounts recognized in the Institute’s financial statements.

• Amendments to IFRS 10, IFRS 12 e IAS 28 “Investment Entities: Applying the Consolidation

Exception” (published on 18 December 2014): the amendments contain changes relating to

issues that arise from the application of the exception granted to the consolidation of investment

entities. The adoption of the amendments had no impact on the disclosures or the

amounts recognized in the Institute’s financial statements.

Finally, as part of the annual process for the improvement of the accounting standards, dated 12

December 2013 the IASB published the document “Annual Improvements to IFRSs: 2010-2012

Cycle” (including IFRS 2 Share Based Payments – Definition of vesting condition, IFRS 3 Business Com- 41

IOR

Annual report 2016

bination – Accounting for contingent consideration, IFRS 8 Operating segments – Aggregation of operating