par Francois de Siebenthal | Déc 30, 2016 | Uncategorized

Versions améliorées. Mise en ligne le 1.01. 2017. Joyeuse année… Le sujet le plus important pour le bien commun de tous.L’ émission de radio courtoisie avec des graphiques, des images et des caricatures, notamment de MM Jude Potvin et Bernard Dugas.Les...

par Francois de Siebenthal | Déc 30, 2016 | Uncategorized

/ / _ __ _ _ __ /–/ / / / /_/ /_/ / // /_/ / / /-/ /__ / /__]/-//__ / 0x? HackBack movement AnD AnonyMous ===============[ present ]================ === Message to the People === SInCe the Advent of Time, huMans have long forgotten to love and CaRe for eaCh...

par Francois de Siebenthal | Déc 30, 2016 | Uncategorized

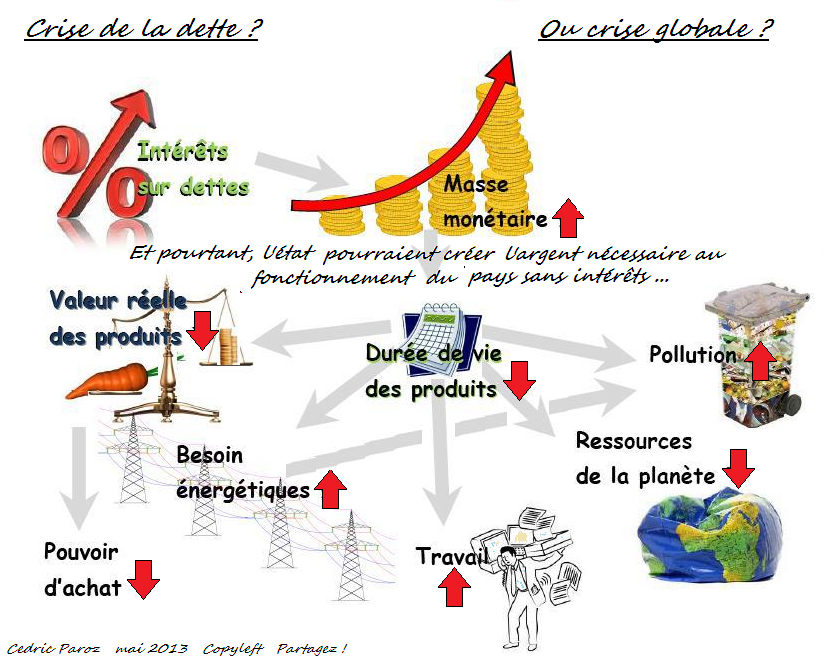

INITIATIVE POPULAIRE POUR UNE RÉFORME MONÉTAIRE “MONNAIE PLEINE” LE MESSAGE DU CONSEIL FÉDÉRAL : UN CONSTAT D’IGNORANCE OU DE MAUVAISE FOI…. OU LES DEUX À LA FOIS ? par M. Christian Gomez, banquier, Dr en économie, membre du Conseil scientifique de...

par Francois de Siebenthal | Déc 29, 2016 | Uncategorized

Les finances du point de vue suisse, la BNS, alias banque nationale suisse, les intérêts négatifs, les monnaies pleines, le fédéralisme et le respect du principe de subsidiarité des 26 états suisses, les facilités monétaires pour les peuples, alias quantitative...

par Francois de Siebenthal | Déc 29, 2016 | Uncategorized

3 heures de radio courtoisie à écouter… Les finances du point de vue suisse, la BNS, alias banque nationale suisse, les intérêts négatifs, les monnaies pleines, le fédéralisme et le respect du principe de subsidiarité des 26 états suisses, les facilités...

Commentaires récents