par Francois de Siebenthal | Juin 30, 2017 | Uncategorized

L’intérêt sur l’argent créé est un vol Notre-Seigneur a chassé du Temple les changeurs d’argentIl est grand temps de chasser les Financiers Internationaux Comme la plupart des lecteurs réguliers de Vers Demain devraient le savoir, le défaut fondamental du...

par Francois de Siebenthal | Juin 29, 2017 | Uncategorized

Gabriel Galice, président de l’Institut international de recherches pour la paix à Genève : “Les Américains ont un plan qui est de remodeler le Moyen-Orient et c’est un projet de prise du pouvoir” Le coup d’état en Syrie organisé dès 2006...

par Francois de Siebenthal | Juin 28, 2017 | Uncategorized

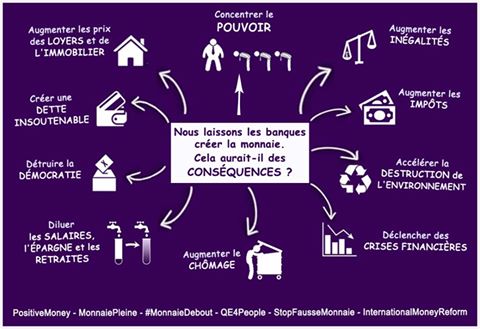

Dear Friends of Common Good, Please, help us to answer to the swissbanking.org, Study: “The Sovereign Money Initiative in Switzerland: An Assessement” (EN) thank you 111’111 + Swiss, positive money & social credit Vollgeld is swiss,...

par Francois de Siebenthal | Juin 28, 2017 | Uncategorized

Dear Friends of Common Good, Please, help us to answer to the swissbanking.org , Study: “The Sovereign Money Initiative in Switzerland: An Assessement” (EN) Thank you 111’111 + Swiss, positive money & social credit Vollgeld is swiss,...

par Francois de Siebenthal | Juin 28, 2017 | Uncategorized

de Kassambre (modifié) +Louis Hannetel : ” mais je ne vois pas comment changer ce système” Cet ex banquier suisse ne se contente pas de dénoncer le système bancaire, il se propose de le révolutionner, avec la conviction, soumise à la...

Commentaires récents