Venue:

We fetch you at the airport. Rougemont is located 50 km east of Montreal,

on Highway 112, between Marieville and Saint-Césaire

1101, Principale St.

Rougemont, QC

Canada – J0L 1M0

The next free training session at the Social Credit and the social doctrine of the Church will take place in Rougemont in Canada in French with instant translation in English, Spanish and Polish, from 27 April to 7 May 2017, followed by our Jericho

Rougemont in Canada

A week of adoration of 8 to 14 May 2017.

——————————– ————————————————-

week of study; translation in French and Spanish, Polish at request.

15 juillet au 21 juillet at Rougemont in Canada 2017

19 juillet : Pilgrimage

22 juillet : Apostolate

23 juillet : 4th Sunday

—————————————————————-

Session d’étude en francais à Rougemont au Canada

21 septembre au 28 septembre 2017

24 septembre- pèlerinage

29 septembre : apostolat

International Congrès in 4 languages at Rougemont in Canada

30 septembre 1er & 2 octobre 2017

You are invited & you can stay 2 or 3 weeks http://desiebenthal.blogspot.ca/2016/08/forum-from-jakarta-to-montreal.html

http://desiebenthal.blogspot.ch/2015/12/swiss-positive-money-social-credit.html

If concepts are not right, the words are wrong,

and if the words are wrong, works cannot be achieved.

Confucius

This prophetic mail was sent in April 2008, copy for you

More and more robots and computers will produce most of the goods. less and less human will be necessary to produce what is neccesary to live, the problem is how to distribute the money to buy all goods on the market ?

Do not accept a centralized system, go the swiss way. Small is beautiful.

Say no to more taxes.

Robert A. Heinlein described a Social Credit economy in his first novel, For Us, the Living (published in 2003, but apparently written ca. 1939). (Beyond This Horizon describes a similar system, but in less detail.) The society in the book uses a method to prevent inflation: the government makes a deal with business owners. Instead of increasing prices, they cut prices, and the government (or the Bank of the United States) pays them the difference after seeing their sales receipts. Like the guaranteed income or heritage checks, this money comes out of the inkwell. In the future, the government no longer uses taxation to fund itself. The characters point out that present “fractional reserve” law allows banks to create money (by loaning out many times more money than they have on hand), while in Heinlein’s future society only the US government can create US currency.

Robert Anton Wilson proposed another form of Social Credit. His plan aimed to end wage slavery, and began by offering a reward to any worker who designed him-or-herself out of a job. The guaranteed income (or, in the Schrödinger’s Cat Trilogy, a lesser reward to all other workers who “lose” their jobs to innovation) would prevent starvation. This income would consist of “trade aids” which would lose numerical value with the passage of time. This official reduction in value would encourage spending and (although Wilson does not state this explicitly) limit price inflation. Elsewhere, Wilson attributed this strategy to Silvio Gesell, who also suggested the government encourage small communities to experiment with alternate economic models. If one of these enclaves seemed especially successful, the country could copy their model in place of Gesell’s own plan.

How you can open an interest-free bank

with the use of simple cards

français

|

|

|

|

|

The principle is the same as in the tale of “The Money Myth Exploded”: an account is created for each member of the community

|

http://pavie.ch/articles.php?lng=en&pg=765

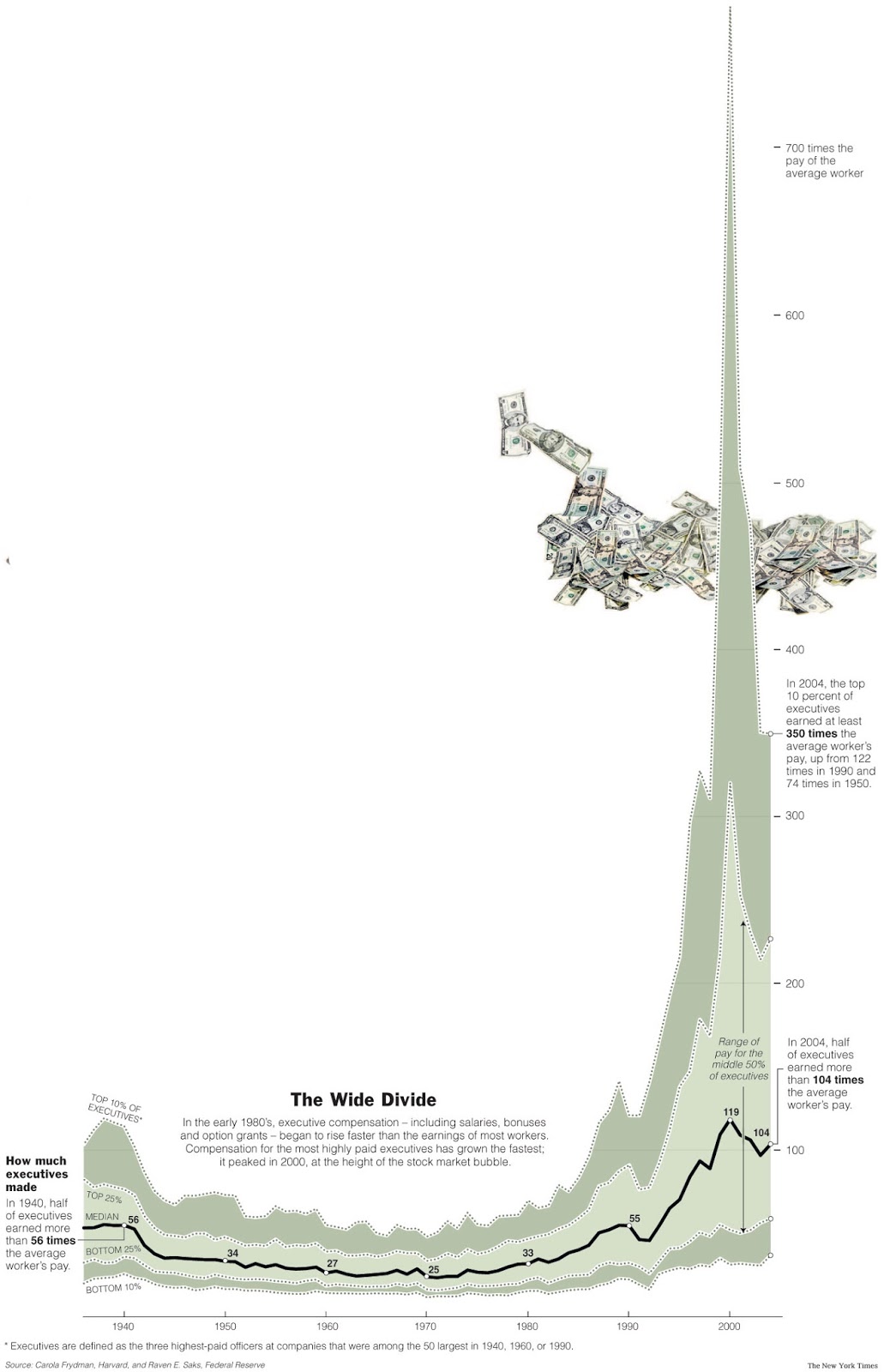

Subprime crisis, a systemic crisis : how to reform the whole system before a massive failure of most currencies?

Is really more centralization and more power to less people earning more millions $ at the expanse of more and more poors the solution ?

What are the roots of the problems ?

Do you find good that a few individuals can earn salaries above US $ one billion per year…( sic, with all bonuses, incentives, stock options…), one hundred million, 20 millions and so on, when others are dying of hunger ?

While large financial assets are growing exponentially and in a continuous manner, debts will increase even much more. It is the responsibility of the working population to generate interest and accumulated interest. This creation takes place directly in purchases – Helmut Creutz, estimates that 40% of the price of consumer goods, at least, are now hidden interests – and in the form of taxes.

The real cost of the interest on public utilities is above 1’000 % ( sic, one thousand per cent)

Even central and local government must provide debt service continuously paying interest and accumulated interest. This development requires an exponential growth of the economy and constantly leads to new crises.

One author, Hermann Kendel from Berlin, describes in detail the propensity to the crisis and the various attempts to moderate. In doing so, he mentioned other consequences of the system of accumulated interest, including the ongoing crisis in the Third World and ecological disaster.

We must work several hours every day to cope with those hidden costs, we have houses 77 % more expansive or smaller, food is twice the price, everything costs too much. 99,9999999 % of the population has to pay those crazy bonuses in New-York to the happy few shylocks…

The US $ has now a value of only 1 swiss franc, from four francs ( 4,47) in 1948, and it will continue to go down. Small is beautiful and Switzerland is very decentralized, we have even the wir system, a private money system. see www.wir.ch

What are they offering ? what “solutions” in one year time ?

Remember, the FED is a private organization, created just before Christmas 1913, the 23th December ( most politicians were already gone to buy presents for their families…), to pass discretly a law to rackett the poorer, at a very high cost, human lifes, wars, revolutions, terrorism.

They create the roots of most troubles.

All the economy is based on loans with interests. Created by a few happy at the cost of more and more poors who are dying.

What are the costs of such a system ? Alcool, drug, psy, depressions, cancers, divorces, abortions, wars, crisis, unemployment…

The main points of the Bush administration’s plan to change financial regulation is more centralization and higher costs to the poorer:

— Expand the role of the President’s Working Group on Financial Markets to include the entire financial sector and not just financial markets. BIG BROTHER WILL WATCH YOU…

— Create a new federal commission at very high costs, the Mortgage Origination Commission, to develop uniform, minimum licensing standards for mortgage market participants.

— Move the Office of Thrift Supervision, which regulates thrift institutions to the Office of the Comptroller of the Currency, which regulates banks.

— Merge the functions of the Commodity Futures Trading Commission into the Securities and Exchange Commission to create one new agency to provide unified oversight of the futures and securities industries at very high centralized costs.

— Establish an Office of National Insurance within the Treasury Department to regulate those in the insurance industry who want to operate under an new optional federal charter, to make more paperwork.

— Divide and conquer centrally. Work to establish as a long-term goal three major regulators: the Federal Reserve as a “market stability regulator”; a “prudential financial regulator” to take over the functions of five separate banking regulators; and a “business conduct regulator” to regulate business conduct and consumer protection.

Solutions:

We need urgently to put a real and true sytem close to the people. We need to recover our responsabilities. The only way is local systems, easy to understand and to control. Act now, join and improve all local initiatives, be the salt of the earth.

We need urgently the revival of the encyclical Vix pervenit to fight against all forms of usury and put Christ in the center of the economy. France has offered a Statue of the Liberty. We launch a general auction to offer a statue of the Responsability to USA, to be built at ground zero for instance.

Kennedy was killed by crooks because he was trying to implement globally this new economy with his order 11110.

We all need God to help us at a family and local level and we need to accept all five sabbats.Lev. 25: 23

| כג וְהָאָרֶץ, לֹא תִמָּכֵר לִצְמִתֻת–כִּי-לִי, הָאָרֶץ: כִּי-גֵרִים וְתוֹשָׁבִים אַתֶּם, עִמָּדִי. | 23 And the land shall not be sold in perpetuity; for the land is Mine; for ye are strangers and settlers with Me. |

1 Timothy 6:10

King James Bible

For the love of money is the root of all evil: which while some coveted after, they have erred from the faith, and pierced themselves through with many sorrows.

The Trader Monthly April/May 2007

John Arnold

City: Houston Firm: Centaurus Energy Age: 33

In a clash of the titans that is likely to be remembered for years to come,John Arnold took on Amaranth’s Brian Hunter last year in a battle over the direction of natural-gas prices. Hunter, the bull, got the horns when prices — along with his ability to trade out of the supremely dark corner into which he had painted himself — weakened in the summer. Arnold, formerly of Enron, squeezed his foe like a laundress wringing out a wet tube sock.

In the end,Arnold and his team of 10 traders — including right- hand man Michael Maggi and natural-gas guru Bill Perkins — walked away from the dustpile with a mountain of cash. Amaranth was wiped off the map.

Arnold claimed the bulk of the profits. He guided Centaurus to gaudy returns (on an estimated $2billion in assets) of 317 percent before fees. Apart from one “lousy”year (only 178 per- cent in 2005), the fund has always finished above 200 per- centsince inception in 2002.

Centaurus’s fee structure is 3-and-30. About half the fund is Arnold’s own money. He is the sole owner of the firm. And — good gosh almighty, what a year — he even got hitched to a beautiful Houston lawyer.

“Last year, it all came down to natural gas,” says one trader familiar with Arnold’s bonanza. “Some people had one idea about what it would do; others backed a different scenario. The bottom line is that a whole lot of money changed hands. When you start hearing from other traders that people are selling bonds just to meet margin, that’s when you know that some positions are too big and it’s all over.”

Arnold declined to comment on our income estimates, as did Centaurus’s Perkins, though Perkins shared his views on why a trading bounty is such a beautiful thing. “You ask a big CEO what he makes, and it’s a huge number, but it’s all tied up in stock and options. Traders get paid in cash. It’s liquid. It’s real. You can go, ‘Here, look,’ and slap someone across the face with it.”

Given Arnold’s record 2006 — the largest sum, we believe, anyone has ever earned in one year — a slap like that just might land someone in intensive care.

City: East Setauket, New York Firm: Renaissance Technologies Corp. Age: 68

Simons is out of control. In 2006, the Long Islander’s $5.7 billion Medallion fund — perhaps the most successful black-box strategy in history and certainly, at 5-and-44, among the priciest — returned a heady 40 percent. Meanwhile, his Renaissance Institutional Equities Fund, already among the largest in the world since launching in August 2005, produced a 15 percent return.

He and his 200 or so employees — many of them Ph.D’s who in another era would have worked for NASA — are rocketing to the industry stratosphere. Simons, himself an MIT grad who began his career as a mathematician and Defense Department codebreaker during the Vietnam War, is now using his fortune to support autism research and to stand up for inner-city math teachers. When we did the math on Simons’s earnings, meanwhile, we nearly fell over.

Eddie Lampert

City: Greenwich, Connecticut Firm: ESL Investments Age: 44

Lampert has put himself firmly in the pantheon of great buyout-fund managers thanks to his proclivity for making correct bets on unloved companies. His bargain-bin pickup of Kmart a few years ago, followed by a smart Sears parlay, continued to play out (on paper, at least) in 2006.

Lampert appears to be turning Sears Holdings Corp. (SHLD) into a Berkshire Hathaway clone, and the market is loving it, pushing the stock up more than 40 percent last year. Lampert’s portfolio is brimming with SHLD, generating more than $2 billion in paper gains.

We’ve struggled with the question of whether Lampert is actually a trader; his lines of enterprise — retail, real estate, private equity, long-term investment — are blurry. But what’s clear is that this former Goldman Sachs intern is making money hand over fist.

City: Dallas Firm: BP Capital Age: 78

The world’s biggest oil bull may have gotten gored in late 2006 and early 2007 as crude prices slipped, but that slide didn’t last long. Besides, his prudent bearish play on natural gas in the fall of ’06 was more than enough to fuel his energy-futures and derivatives fund to a startling 98 percent return.

“Most of our money came from shorting natural-gas futures,” says Dick Grant, BP’s CFO. The firm’s total assets, across two main funds, are around $3.6 billion, 45 percent of it Pickens’s own money. Grant wouldn’t confirm Pickens’s take, but if our estimate isn’t pretty close, we’ll build Oklahoma State a new football stadium.

Stevie Cohen

City: Stamford, Connecticut Firm: SAC Capital Advisors Age: 50

Despite some fairly sinister media coverage of allegations stemming from a lawsuit brought by Biovail, Cohen remains one of the most powerful forces in equity trading and is still the man every sell-side sales guy on the planet wants to serve; his Death Star of a hedge-fund operation flirted with $11 billion in assets at the end of last year.

We first heard that Cohen banked around $800 million in 2006 — a plenty good year as is. But as we dug for further information, we discovered that his fee-revenue pool, based on calculations and some reasonable assumptions, easily surpassed $2 billion and might even have edged up near $3 billion, with all his big funds up more than 30 percent.

Of course, we don’t know for certain that his monster kitty came in at more than $2 billion. And we can’t automatically assume that he took half for himself. But it’s a good hunch.

Stephen Feinberg

City: New York Firm: Cerberus Capital Management Age: 47

Feinbergs’s Cerberus assets under management, a mix of hedge and buyout funds, exceed a staggering $22 billion. Without splitting hairs, we’ll simply say Feinberg more than holds his own among trading icons. Besides, who doesn’t straddle the line between private equity and trading these days?

The Cerberus International fund, with around $5 billion, scorched in 2006, returning around 21 percent. Feinberg’s victory over KKR in the GMAC deal was the stuff of financing legend, while his BAWAG bailout was another cool-handed move by this Drexel alum.

Paul Tudor Jones

City: Greenwich, Connecticut Firm: Tudor Investment Corp. Age: 53

From his humble beginnings as a cotton-futures trader, Jones has grown his hedge-fund empire to more than $15 billion. Meanwhile, his annual Robin Hood Foundation charity event (which last year raised $48 million in a single night) has become so large it’s now held at the Javits Center.

Jones still personally manages his global fund, which has around $5 billion. That fund (with an off-the-top fee of 4 percent of assets and a 23 percent cut of profits) had a rather pedestrian 11 percent return last year.

But take into account that as majority owner of the firm he gets a healthy portion of the revenues from the other funds and that he has a substantial amount of his own money invested, then factor in a prop-trading vehicle that reportedly generates hundreds of millions more, and . . . well, vertigo ensues.

City: New York Firm: Caxton Associates Age: 62

A Macro trader’s macro trader, Kovner returned to form in 2006 following three consecutive years of single-digit returns. The Caxton Global Investments fund, with more than $7 billion, returned around 12 percent.

This well-known music lover (and neoconservative), who last year gave the Juilliard School his vast collection of original sheet music from the likes of Beethoven and Mozart, conducts a multi-strategy symphony of portfolio stewardship incorporating stocks, currencies and commodities.

Israel Englander

City: New York Firm: Millennium Management Age: 58

The man known as “Izzy” has a hand in the positions taken on at Millennium, which has $9 billion in assets. The Millennium Capital fund brought home a 17 percent gain in 2006, besting most of its peers. Commanding a 20 percent cut of profits, the Brooklyn-reared Englander — who dropped out of the MBA program at New York University, got his start on the floor of the American Stock Exchange, became tangled up in the Ivan Boesky scandal and started Millennium in 1989 with $35 million — truly cleaned up last year.

His performance, in other words, made a rounding error of his roughly $30 million payment tied to the December 2005 settlement of mutual-fund market-timing charges brought against him by the SEC.

City: New York Firm: D.E. Shaw & Co. Age: 55

Lording over one of the biggest quantitative hedge funds ever created, Shaw is a trading legend who casts an equally substantial shadow in private equity. A former computer-science professor at Columbia, Shaw relies upon computer-generated investment strategies aiming to capitalize on market anomalies.

These methods remain a mystery, but with $29 billion under management, a 3-and-30 fee structure and impressive returns, Shaw’s earning power, it’s safe to say, is seldom rivaled.

More on:

http://userpage.fu-berlin.de/~roehrigw/creutz/geldsyndrom/english/index.html

http://userpage.fu-berlin.de/~roehrigw/kennedy/english/

* http://www.reinventingmoney.com

* Margrit Kennedy: Why Do We Need Monetary Innovation? (pdf, 20 Seiten)

* Helmut Creutz: The Money Syndrome

* 2000: Werner Onken: A Market Economy without Capitalism

* 2000: Eiichi Morino: A Story of Robinson Crusoe (by Silvio Gesell) as a Manga

* 1998: Jürgen Probst: Aberrations of an interest-based economy

* 1995: Erhard Glötzl: The How and Why of a New Monetary System

* 1995: Margrit Kennedy: Interest and Inflation Free Money

* 1990: Dieter Suhr: The Neutral Money Network

* 1941: Vincent C. Vickers: Economic Tribulation

* 1934: Michael Unterguggenberger: The End Results of The Woergl Experiment

* 1933: Irving Fisher: Stamp Scrip

* 1920 (?): Silvio Gesell: Natural Economic Order (Link http://www.systemfehler.de/en/ )

| 2 pièces jointes — Télécharger toutes les pièces jointes Afficher toutes les images | |||

|

|||

|

|||

—

Pour nous soutenir, mieux résister aux manipulations, rester unis et recevoir des nouvelles différentes et vraies, un abonnement nous encourage. Pour la Suisse, 5 numéros par année de 16 pages par parution: le prix modique de l’abonnement est de 16 Sfr.- par année (envois prioritaires)

Adressez vos chèques à:

Mme Thérèse Tardif C.C.P. 17-7243-7

Centre de traitement, 1631-Bulle, Suisse

The Debt Brake

Chancellor Angela Merkel confronts growing criticism for her one-sided emphasis on cutting expenditures of the state as a recipe for the troubled situation in Greece and other Southern countries of the Euro-zone. The most successful blogger in France on contemporary economic processes, Paul Jorion, called her fiscal pact, vulgo “debt brake” a “blague de potache” or “schoolboy prank” (and here again in German) and the Nobel laureate Joseph Stiglitz calls it suicidal for Europe.

Every now and then Mrs Merkel refers to the example of a Swabian housewife who reliably and responsibly keeps her house in order. A clue for the rationale behind might be found in the “Song of the Bell” by the poet Friedrich Schiller (being born in Swabia himself) more than 200 years ago:

… And inside rules

The prudent housewife,

The mother of children,

And wisely reigns

In the domestic circle,

And teaches the girls,

And guides the boys,

And stirs without end

The industrious hands,

And multiplies the gains

With orderly mind…

By the way, Mrs Merkel here also follows her mentor, the former Chancellor Helmut Kohl, who expressed his basic understanding of economics with words like: “What is right for an individual household, can not be wrong for the state’s budget.” Of course, he is right, this is pretty well applicable to the state’s administration and to any individual business, but it cannot serve as a guideline when facing the complex interplay in a national economy with millions of individual enterprises and households. This requires a more profound knowledge of how to harmonize the millionfold different wishes and aspirations on a basis of fairness and justice. But as a business economist doesn’t see the forest because of the many trees, the national economist sees the forest but cannot distinguish individual trees. They are living on different planets.

Dirk Müller, an investment consultant and stock broker, managed to break a taboo in the public discussion in Germany by introducing the problem of compound interest in mainstream media. He gives a neat explanation why the restricted view of a Swabian housewife, i.e. the managerial-economics of entrepreneurs, of the state or any other individual participant in the economy, cannot account for macroeconomic interrelations. He points at the total indebtedness and its root cause in national economies.

Business Management vs. Macroeconomy

The trouble is, that debtors, who manage to repay their loans, repay it to the bank where they got it from. The banks in turn credit the repayment plus interest to the accounts of the owners. Multi-millionaires and billionaires, even if they wanted to use their money for consumption, would simply be unable to spend it all. Thus, the monetary assets remain in the system and the banks have to find new debtors who are creditworthy enough to earn the interest, which the banks owe to the owners of monetary assets. In the long run, this becomes more and more difficult as monetary assets and the respective debts grow. Therefore, the banks increasingly turned to speculation in order to gain the necessary means for servicing the monetary assets. For that purpose they have also invented obscure new financial instruments. To put it short: the total indebtedness remains in the system and increases, regardless of individual debtors repaying their debt. Banks which suffered from losses in speculation, called for bailouts only in order to maintain liability towards their obligees.

The following graph is taken from The Money Syndrome. The figures here are a bit more accurate than the ones Dirk gave in his talk. The orange column represents the average annual income of an employee or household, while the greenish column represents the per capita share of the total indebtedness.

In the fifties an average citizen had to pay 6% for interest in prices and taxes and for private loans. This share of his income went on top of the monetary assets of some creditors. And at the same time it increased the total of indebtedness, because the banks which collected these interest payments had to find new creditworthy debtors. In the mid-seventies the debt share had already doubled and so did the interest burden which then amounted to 13% of an average household income. In 2000 the interest share doubled again to 28% and today the share amounts to over 40%. Note, that all interest payments only increase the indebtedness which again leads to an increase of interest demands. This happens with accelerated speed. It’s a vicious circle, which finally and inexorably leads to a collapse of the whole system. Ask the economic experts what this system is good for! And the Swabian housewife may “wisely reign in the domestic circle” but she doesn’t know what’s going on outside and how her inside reign is getting affected despite her diligent care.

Every Homogeneous Region Needs a Suitable Currency

In the following video Dirk Müller points at another important factor, which the Euro doesn’t account for and more or less cripples the members of the Euro-zone because of a basic flaw in the Euro system.

It is a fact, that nations dispose of different economic capacities. The reasons for that are manifold. It depends on disposable resources, developed infrastructure, communication and traffic facilities, efficient administration, skilled craftsmen, social structure, education, culture a.s.o. Such differences cannot only be observed between nations, but also in various regions within a nation. Germany for instance is a federation of 16 states. Dirk Müller’s example referred to the difference between the poor Saarland and the rich Baden-Württemberg. In larger states like Bavaria such a difference can also be observed between the poorer North and the richer South of Bavaria. The established practice to deal with these differences is a transfer of payment from the richer states to the poorer ones. This is feasible because these more or less autonomous 16 states are politically united and the differences are bearable. And yet, these transfers are a constant source of conflicts between states, which have to be negotiated once and again to find a compromise. Just recently the chief minister of Bavaria moaned about “too high” transfer payments to other states. The effect of these transfers is quite similar to the effect of development aid to Third World countries, where these financial infusions create a dependency on the helper and often keep them in a persistent state of vegetating and doesn’t allow them to achieve real autonomy. Besides, the existing money system has a strong tendency to concentrate in hotspots and the subsidies soon flow off again to those concentration spots – via industrial conglomerates, large international corporations, international trade chains a.s.o. Countries, which have to deal with this predicament again and again, are often referred to as a bottomless pit. Particularly rural areas everywhere in the world are suffering from money drainage, which commonly is blamed upon “globalisation”. But that’s a misunderstanding. The world’s money system is outdated. It was devised at a time when our ancestors wanted to explore and conquer a world, the size and extension of which they had no idea. The age-old core of the money system remained unchanged, although we know the limits of our world today. We have to acknowledge these limits in order to get beyond them and find a sustainable way of life. This is impossible with an obsolete money system and a stubborn belief that this system could go on for ever.

Marek Belka, the Governor of the Polish Central Bank just recently came up with a proposal for Greece’s dilemma (Financial Times Germany). Greece’s problem with the Euro is: it cannot be adjusted to its economic capacity, i.e. devaluated. He therefore suggests a dual currency system for Greece: the savings of citizens would be deposited in banks with the stable Euro, while the internal currency, issued by the state, would be used in the real economy. Wages and salaries would then be paid with a heavily devaluated special “Euro”(?). The proposal of Chief Macroeconomist Thomas Mayer of the Deutsche Bank (in English). goes in a similar direction: a heavily devaluated parallel currency (“Geuro”) as a temporary measure. These two proposals and some others imply, that, after a transitory period, Greece could go back to “normal”, resume the Euro and the compound interest system… and everything would be fine then?

A Europe of Autonomous Currency Regions…

Greece may be blamed for a chaotic administration of its economy, but it is not responsible for the weak design of the Euro system, which can not integrate heterogeneous economies unless they converge in a set of economic parameters. It is designed for a homogenous economy and may well serve for a country like Germany, but it cannot account for the special features of a multitude of European economies. Even the Deutschmark could not account for the different conditions in all regions and required transfer payments from the stronger parts to the weaker ones. Germany’s “transfer union” is a patchwork solution and cannot serve as a model on a European level, because the differences between nations are much greater.

Christian Gelleri and Thomas Mayer are the initiators of the “Chiemgauer” (please note: the Chief Macroeconomist of the Deutsche Bank and the “Chiemgauer” initiator Thomas Mayer incidentally share the same name but not the same identity), a regional currency in Southern Bavaria. It was founded in 2003 and so far it’s the most successful Regio project in Germany, which will celebrate its tenth anniversary in 2013. The initiators submitted a proposal that could not only Greece’s economy get back to work, but could be a first step to overcome the outdated money system and open the perspective of an economic order that meets the needs of today and a long future. They have elaborated their proposal in a working paper which can be downloaded as a PDF-file in English, German, French, Portuguese and last not least in Greek from Eurorettung.org (translations in more languages are planned). The original idea of the Regio was to strengthen the regional economy and to protect it against the drainage of Euros. The Chiemgauer is therefore endowed with a circulation incentive as most other Regio initiatives in Germany which keeps it running and sustains the robustness of the regional economy. The Regios are devised as complementary currencies which do not aim at replacing the Euro, but as an additional instrument which allows more autonomy to homogeneous regions. These homogeneous regions may be of different size, roughly speaking within a range of 3 to 15 million or so households. As a complementary currency Regios could everywhere in Europe (or the world) enhance the autonomy and robustness of the respective region. And a Europe of economically robust regions would result in a robust European economy.

… and the Euro as a Supraregional Currency

By no means should the Euro be abandoned! No one in the Euro-zone wants to get rid of the advantages it offers, the Greeks don’t want it and no one else. Currently, the Euro has dramatically lost attractivity and at present no one would like to join the Euro-zone. The Euro system might regain attractivity, if it opened perspectives for overcoming an outdated currency design. Provided the Regio idea spreads all over Europe, the Euro might become the roof over all these currency regions. The Euro would then become a stable supranational or rather supraregional currency unit defined as a standard of reference.

John Maynard Keynes submitted such a proposal for an international clearing union at the legendary international conference in Bretton Woods 1944. It was turned down, though, by the US-American White plan, which favoured the US Dollar as an international key or reference currency. But a national currency is not a good idea for a reference currency. In a way it was advantageous for the USA, if a huge foreign trade deficit can be called an advantage.

Keynes devised the “Bancor” as a supranational currency and one of its major tasks should have been to watch the trade balance between nations and, if necessary, to impose pressure on those whose foreign trade accounts are seriously imbalanced or for too long a time. The advantage of a supraregional currency unit is, that imbalances don’t have to be cleared (although it is possible) on a bilateral basis between peer regions but only between each member with the clearing union. Some of the tasks Keynes had described for the international clearing union, have been realised by the IMF.

If the Euro assumed the role of a reference currency, then each member region would have a suitable exchange rate to the Euro. In the case of changing economic conditions, the exchange rate of the Regio could easily be adjusted accordingly, while the Euro remained stable. This would give the regions a cushion, a certain flexibility and they wouldn’t be compelled to comply with an externally predetermined economic standard of performance. Enterprises which export their products to other regions and travelers through Europe could use the Euro as a means of payment as they do today without having to worry about regional exchange rates.

Mainstream Economics – an Outdated System

Economics is not a natural science, but is usually understood as a part of social sciences. Although social sciences focus on different phenomena or take a different point of view, they also have to account for relevant natural laws and cannot simply ignore them. An apt metaphor for the complex economic processes in a live community might be the metabolism of living beings. Metabolism describes the biochemical changes of matter for building the body’s own components, for gaining thermal and kinetic energy, for abandoning faecal matter and by coordinating these cyclic processes through information feedback via the nervous system. Economy might be seen as an extension of individual metabolism to regional, national or even global size, the possible performance of which surpasses the capacity of an individual.

Alas, today’s economic science cannot provide a basis for the organisation of a sound economy. A conspicuous example for the incompetence of economics is the LTCM (Long-Term Capital Management), founded in 1994. The hedge fund worked with theories that were elaborated by two professors, Robert C. Merton and Myron Scholes, who received the Nobel Prize 1997 “… for a new method to determine the value of derivatives.” In its heydays the hedge fund commanded more than 100 billion USD in assets and showed a return on investments of over 40%(!) per annum. Then the Russian Financial Crisis occurred, and Russian Government Bonds, which the LTCM held as security, lost their value. At the end of 1998, the Fed organised a bailout with a number of business partners of LTCM in order to avoid a wider collapse of financial institutions in the US and beyond. Some time later the French Nobel laureate Maurice Allais was asked, what was going wrong, where had Merton and Scholes made a mistake in their calculations? And Allais answered: “The mathematic equations were perfect, there was no mistake. Reality was wrong!” Note the irony in the statement: reality should submit to economists’ fancies?

Many years ago, Congressman Ron Paul once asked Alan Greenspan, then Chairman of the Federal Reserve Bank, “What is money?” Greenspan quite frankly admitted, “I don’t know. But we are working on it.” Money, which we are using today, is primarily issued on the security of the state’s treasury bonds, i.e. on the promise to repay it some time in the future. But that day may never come, as John Kenneth Galbraith pointed out:

“In numerous years following the war, the Federal Government ran a heavy surplus. It could not, however, pay off its debt, retire its securities, because to do so meant there would be no bonds to back the national bank notes. To pay off the debt was to destroy the money supply.”

What information does a money carry, that is issued on a vage promise which will never be delivered? It invites all sorts of speculations about its value and this is happening as long as idle money is roaming around on the globe with the effect, that Keynes so aptly described:

“Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation.”

The information of money at the moment of issuance is in direct contradistinction to the money that is circulating in the realm of real economy. Someone who accepts money for a work done is then entitled to claim equivalent goods or services that are offered in the market. This is the comprehensible information of money circulating in the real economy and it is maintained at every change of hands. However, the circulating money, too, does not account for the loss in the market, as long as it is held idle. This is where thermodynamics comes into play to compensate for this loss and keep the economy running.

Thermodynamics is a special branch of physics. Historically, it emerged in the beginning of the 19th century as a new approach to deal with energy conditions, transformation from one kind of energy to another or changes of energy states. At the beginning of the 20th century it gained increased relevance in fundamental scientific research, quantum physics, chemistry and biology. Entropy is also applied in information theory and social sciences.

Silvio Gesell, Rudolf Steiner and J.M. Keynes probably had not studied thermodynamics, but they must have had an intuitive insight when talking about “rusting money” (Gesell), “ageing money” (Steiner) or “demurrage fee on liquidity” (Keynes). The circulation incentive in today’s regional currencies accounts for a natural law described in thermodynamics and could therefore become a feasible and smooth transition from an outdated money system to one that can really meet the global challenge. A more detailed explanation of the 2nd Law of Thermodynamics and its application in economics would go beyond the scope of this article. But it will come in one of the next articles.

A New Europe?

Robert Mittelstaedt

Greek Tragedy

July 30th, 2011

There is a tale in Greek mythology about the daughter of a Phoenician king who was seduced by Zeus in the disguise of a bull. Her name was Europa. A whole continent inherited this name. Yet this is just a symbol for the rich heritage of arts, science, philosophy, drama, which shaped the culture of this continent from its cradle onwards. More than 2500 years ago the Greeks invented the phonetic alphabet, from which the Latin and Cyrillic letters were derived. At around that time a cultural revolution happened, which is associated with the names of outstanding personalities still well known: Pythagoras, Euclid, Archimedes for mathematics and natural science, Socrates, Plato, Aristotle for philosophy, in order to mention just a few examples. The Greek dramas dealt with themes of universal relevance and are still an inspiration in our time. The theme of Sophokles’ “Antigone”, for instance, is the conflict between the law of a ruler and individual human dignity and conscience. Another of his dramas is the famous “Oedipus”, which deals with the seemingly inescapable consequences of a self-fulfilling prophecy. The modern French multi-talent Jean Cocteau elaborated this theme in his adaptation of the Oedipus saga and gave it the title “La machine infernale” (The Infernal Machine). And last but not least, the ideas for the shaping of a peaceful human society – democracy – originated in ancient Greece. The contribution of Greece’s most excellent minds to the making of this continent and their influence far beyond cannot be over-estimated. And there can be no doubt that Greece is an indispensable part of Europe.

Today, Greece is in serious troubles. Moneywise. It’s staggering along the brim of insolvency and needs urgent help. The rest of the euro-zone is alarmed, because it sees the euro-currency at stake. This goes even so far, that Ben Bernanke, President of the Federal Reserve Board, paints a gloomy picture: if Greece’s problem is not solved, this might have devastating effects on the world’s economy as a whole. The flap of a butterfly that triggers a storm. Greece’s administration may be somewhat inefficient and maybe even corrupt to some extent, but this is a minor part of the problem. The concern of the affected neighbours in the euro-zone is the stability of the euro. Their dilemma is quite aptly described in the satirical YouTube-video:

Clarke and Dawe – European Debt Crisis

Although this is quite a funny dialogue, one’s laughter might get stuck in the throat by the end. The crucial question in this video was: how do broke economies get the money for the bailout of other broke economies? And there was no answer to this question. Are all European states broke? How about Germany, which has taken the lead in negotiating the Greek problem within the triad involved: the European Central Bank, International Monetary Fund and European Commission? After all, Germany is still enjoying an AAA from rating agencies. Can this be called a broke economy? Well, we have to differentiate between the real economy and the state represented by its administration. The rating agencies evaluate only financial instruments like treasury bonds issued by the state. In the case of these treasury bonds (a rather euphemistic term, more appropriate would be: debenture bond) the condition of the real economy plays a role in rating, too. At the moment Germany’s economy booms, the state will collect high tax revenues and is therefore deemed capable of servicing its debts. That seemingly justifies a triple A rating.

The thing looks different if we consider the stock of debts. Within 60 years the German state has been piling up debts amounting to 2 trillion or 2,000 billion euros. The servicing of these debts, i.e. interest payments, swallows about one fourth of the annual federal tax revenues. It’s the second largest item in the budget, tendency rising. A few months ago – the state’s debts amounted to 1.8 trillion euros – I have then tried to find out how long it would take and how much it would have to pay, in case Germany would seriously consider to get rid of its debts. I applied the annuity calculation at a fixed repayment rate. The monthly amount for servicing the debts is 4.5 billion euros at an assumed interest rate of 3% (actually it is 3.4%). Since this amount only services the debts, the monthly rate must be higher if the debt is to be reduced, let’s say, 4.6 billion euros. It would then take 125 years to clear the debts and the repaid amount would be about 3.5 times as large as the actual debt sum. Until today the tax-payer was not charged with the servicing costs, because the state made its payments by taking on new debts. That’s how the indebtedness has accrued during the past 6 decades. But this time the tax-payer would have to be directly charged with additional 4.6 bn. per month apart from the normal tax load. Alas, in the meantime the monthly rate for merely servicing the debts has gone up to 5.7 bn. And the state is taking on new loans in order to hide the fact, that it is bankrupt since decades and to make the tax-payer feel as if everything was fine.

Over-indebtedness is a worldwide phenomenon, virtually all states are suffering from this predicament. And even though governments know that this problem has to be solved, no one has a solid plan for getting rid of debts much less is anything effectively done about it. A similar predicament arises from the same structural mismanagement in nuclear power plants. Since 30 years they are producing thousands of tons of radioactive waste without having solid plans for its treatment. And while a sensible solution for the problem is postponed and postponed and postponed the piles of radioactive waste are growing bigger and bigger and increase the danger of accidental or deliberate (e.g. by terrorists) pollution. The same structural pattern of behaviour applies to the financial sector of national economies.

The mechanism for the accelerated growth of indebtedness and corresponding monetary assets – a veritable infernal machine – is described in full detail in “The Money Syndrome” by Helmut Creutz.

Now, Wolfgang Schäuble, Germany’s Minister of Finance, tries to involve private creditors for tinkering an emergency parachute (“Rettungsschirm”*) for Greece. At first glance it seems a sound idea to have creditors waive a part of their claims. After all, some of these creditors have made good profits at the cost of the Greek state. The trouble is, they can’t be made to do so, because there is no law to compel them. They can only be asked to give some of their profits back on a voluntary basis. So, who should ask the creditors and who of the creditors should be asked? Private banks may be among the profiteers, but their main task is to administer the funds of their clients and to play a role as mediators between creditors and debtors. They are obliged to their clients, in particular to the creditors. But they know who the big winners are and they could ask them. Would they? I don’t know, but let’s have a look where the big winners could be found.

Firstly, in contrast to a widespread misconception, we must understand that as consumers we all pay interest even though we have not taken a loan at all. Loans are an important tool for investment and for overcoming temporary liquidity shortages in the economy. The state is not the only debtor in the economy but the largest debtor and the only one who pays interest by taking on new debts and never repays its debt. Private entrepreneurs repay their debts and calculate all arising expenses into the price for their produce including accruing interest. Therefore all consumer prices contain an interest share that may vary within a broad range between 10 to 70 per cent depending on the amount of capital employed for production. On average today’s consumer prices include an interest share of at least 40 per cent.

The following graph is taken from the book “The Money Syndrome“. It shows the market participants divided into 10 groups according to their disposable income and the amount they are using for consumption per year (the green columns). The orange columns indicate the interest payments hidden in consumer prices and the blue columns show average interest returns that the members of the respective groups receive from owning an interest bearing asset.

The following graph is an extraction of the above figure and shows the balance of interest payments and interest yields. The balance of group 9 is almost even. The members of this group own interest bearing assets worth at least 450,000 euros, which yield as much interest returns as they pay while annually spending 50,000 euros for consumption. All lower groups have smaller assets the returns from which don’t suffice to compensate for the losses in consumption. Therefore, their balance is negative. Only group 10 has a positive balance and collects what the majority of market participants (groups 1 to 9) lose in this game. The growing gap between rich and poor is often referred to in the public discussion, but no one ever asks how it is caused. At any rate, primarily the creditors in group 10 should be asked to contribute to the emergency parachute for Greece, because they are the winners in the game.

This system of compound interest is the basic mechanism for redistributing wealth from the poor to the rich. Mathematically, compound interest is an exponential function, which inexorably leads to a crash of the financial system. Nothing can be done to prevent this crash. All measures that had been taken in the current financial crisis only served and still serves to uphold the existing system. It’s not a matter of doubting the willingness of responsible politicians to try their hardest for finding a solution to the Greek dilemma. They are trying to do so on the premises of current economic thinking. And whatever measures they may come up with on these premises will not prevent a devastating outcome, because it is based on the ignorance of a systemic flaw. The thinking of the majority of economists is conditioned in an obsolete view of how the economy works and they cultivate a blindness for the fundamental flaw in the system. This led Dr. A. Bartlett, a physicist, to the conclusion: “The greatest shortcoming of the human race is our inability to understand the exponential function.”

I found at least the statement of a well-known German banker, Josef Ackermann, chairman of the board of the Deutsche Bank. In an interview with the Frankfurter Allgemeine Zeitung (FAZ, June 30, 2009) he made a statement, which may give a hint as to the direction in which to look for a better system.

Ackermann: Conventional theories are essentially based on a static model of equilibrium, in which all transactions occur simultaneously – i.e. time does not play a role. Money only appears as a kind of veil over the real economic activity, but doesn’t have a relevant impact. Similar things can be said about portfolio-theoretical and monetaristic approaches…

FAZ: These theories make a bet without considering time, so to speak.

Ackermann: If processes are considered in time – e.g. money can be spent only after being earned -, this leads to different conclusions. Then money and the creation of money play a central role. Until today this has been neglected in conventional models. Not at last the current financial crisis has shown, that the effects of the money sphere on the real economy are still insufficiently investigated.

Hans Eichel, a former Minister of Finance in Germany, was once asked by a pupil: „How does money come into existence?“ His concise answer is in perfect accordance with the established practice: „We borrow money from ourselves and we pay it back to ourselves.“ This doesn’t really answer the question, though, because the one, from whom I borrow money, should have it already, otherwise borrowing would be futile. So, where does money really come from?

The established conception of money rests upon the belief, that the market participants of a national economy have a potential to create values out of nothing by performing labour. That’s the state’s treasure. In order to excavate this treasure, the state issues “treasury bonds”, whereupon the central bank issues money, which starts and supports the economic process, i.e. the seizure of the treasure. However, treasury bonds of the state are only backed by a promise for future actualization. While the market participants incessantly create values and sustain the economic process, the state (i.e. its administration) goes on issuing promise after promise and fails to fulfil its promises until it finally loses trustworthiness and goes bankrupt. Usually, the state is blamed then of having lived beyond its means. But that’s not true, the normal citizens are not to be blamed for the bad job of their representatives, the politicians. This is what happened in Greece now. In this respect Greece’s economic fate maybe considered as an omen and sooner or later all states which are based on this monetary conception, i.e. virtually all states of the world, are going to run into the same trap. Ben Bernanke might be right. But it’s not Greece which causes a disaster of such a dimension. Instead, a tremendous worldwide tension has built up from the inherent systemic flaw of the system as never before in history, which only needs to be triggered by a butterfly’s flap in order to crash.

Let’s have a closer look now at Ackermann’s suggested alternative: “money can be spent only after being earned”. This is fully compliant with the everyday experience of the vast majority of market participants, who accept money as remuneration for accomplished work, which in turn entitles them to purchase equivalent services or goods that are offered in the market. The conception does away with promises, it has nothing to do with credit or debenture bonds, but acknowledges and documents what actually exists, here and now. And Eichel’s answer to the pupil’s question would sound quite differently, too: “We acknowledge each other’s performances, document them with the useful tool called money and exchange goods and services with it.” This ties money to actual processes, while Eichel’s original answer is a circular argument which ignores any link to the real economy. In contrast to the established practice where money is “backed” by debts, money would then be backed by actual goods and services that are offered in the market for sale.

Ackermann’s complaint about neglected investigations into the impact of the financial sphere on the real economy concerns the credit and interest system. In a situation, when the economy is in a boom cycle, banks generously grant credits to companies and consumers, because it’s quite likely that credits get repaid inclusive interest payments, although in such a situation the demand for credits is lower. But the granting of credits and engaging in investments is their main business and of course they are trying to partake in the situation. In bust cycles, however, banks become parsimonious and meticulously investigate the applicants’ ability to repay. The banks’ behaviour is pro-cyclic, i.e. they support a booming economy and they obstruct it in a bust cycle. This is not in favour of a sustainable economy and has a lot to do with the interest system and also with the state’s indebtedness. Interest has to be paid, no matter in what a condition the economy is. After all, this is the law and it’s a man-made law. And interest rates are always positive, even if the economy cannot earn enough to pay for them. Therefore, in a recession, the state is required to take over the idle capital by taking on debts in order to boost the economy. After all, the state enjoys a high degree of creditworthiness and is (was) deemed unable to go bankrupt. This keeps interest rates in a positive range, even though and particularly in a saturated economy they should be allowed to decline in market conformity to zero or temporarily even below zero. Thus, the state itself gets under pressure for increasingly being unable in the long run to reduce its debts in an orderly way. A state at the brim of insolvency like Greece, being classified as C by rating agencies would have to pay interest at an usurious rate of around 20% which would eventually destroy not only the state but the economy as well.

This is the special feature of our established capitalist system, which Heiner Geißler, social politician of the Christian Democrats, has concisely characterized: “Capitalism is theft endorsed by the state.” His associate of the CDU, Angela Merkel, in negotiating the “emergency parachute” for Greece and possible other members of the EU with experts of the IMF, ECB and European Commission, did so with the declared intent to go to the roots of the problem. That was a slightly immoderate statement, though, considering the outcome of these negotiations. The “emergency parachute” or by its official term “European Financial Stability Facility (EFSF)” is still far away from the roots of the problem. Thorough investigations into the impact of the financial sphere on the real economy are still badly needed and long overdue.

The Greeks cannot be blamed for having invented the interest system. They can even refer to one of their outstanding ancestors, Aristotle, who clearly described the nature of interest:

“Money was intended to be used in exchange, but not to increase at interest. And this term interest, which means the birth of money from money, is applied to the breeding of money because the offspring resembles the parent. Wherefore of all modes of getting wealth this is the most unnatural.” (I.1258b4 – Wikiquote: Aristotle)

I have met Cassandra the other day and she, being a well-known figure in Greek mythology, too, said with a gloomy look in her eyes and a voice pregnant with meaning: “Capitalism is doomed!”

I know. But who would listen to her and give birth to an insight?

By Robert Mittelstaedt

The UK Edition of “The Money Syndrome” is out!

August 10th, 2010

If you are interested in obtaining a print copy of “The Money Syndrome. Towards a Market Economy Free from Crises” by Helmut Creutz, please go to this website:

Illuminating the Hidden Forces of Our Monetary System

January 15th, 2010

Interview with Helmut Creutz on the English edition of his book, The Money Syndrome

What do readers learn in The Money Syndrome that they do not read in standard economics books?

Readers learn everything essential about money and its functions. You might wonder why that should be of interest to you. You might say that you deal with money on a daily basis, and that there is nothing left for you to learn. Yet, most of us do not grasp the problematic effects of our contemporary money system. Above all, it is the aim of the book to educate readers about the systematic flaws of a monetary system that operates with permanently positive interest rates. And that is something you do not normally read about in standard economic textbooks or magazines. By the way, an economist classified The Money Syndrome as a standard work immediately after its release in Germany. Anyway, while reading the book, you will learn in detail that:

Financial assets accumulate exponentially as a consequence of the compound interest effect.

The indebtedness of private and public households and the economy must grow correspondingly, as financial assets must flow back into the economy as credit.

Interest flows grow similarly in the course of escalating financial asset and debt accumulation. However, financial assets are unequally distributed.

Consequently, the escalating interest flows reallocate capital from those parts of the population that pay more interest than they receive to those that receive more than they pay.

The divide between the rich and poor widens.

Economists and politicians only regard economic growth as a solution to prevent the divide between the rich and the poor from widening.

However, given the finite resources of this planet, constant economic growth – demanding a perpetual increase of production and consumption – is ecologically unsustainable.

Above all, The Money Syndrome not only provides an in-depth analysis of the negative effects of constantly positive interest rates, but also presents a solution: Stabilize the monetary flow by introducing carrying costs to money, as argued by Silvio Gesell.

How did you come up with the idea of writing the The Money Syndrome?

I have been active in environmental and peace initiatives since the 1970s. Back then, I was already looking for reasons why politicians and economists demand constant economic growth despite its devastating consequences. In 1980, a reader of my books gave me a hint. He claimed that underlying processes in our monetary system explain why we ‘need’ perpetual growth. Initially, I was very skeptical. However, trying to show the reader that he was mistaken, I actually discovered that plenty of statistical evidence suggested that he was right! In 1984, I published my first research results in the “Journal for Social Economy” (“Zeitschrift für Sozialökonomie“). One year later, I published a more detailed account of my findings in the article “Growth Till Self-Destruction” (“Wachstum bis zur Selbstzerstörung“). Further research and specification of my ideas led to the first edition of The Money Syndrome in Germany in 1993. Since then, the edition has been revised and translated into several different languages. The work for the French publication was finalized in 2008.

What surprised you the most while researching and writing The Money Syndrome?

Examining statistical series, I was very surprised about the developments in the real economy compared to the expansion of financial assets and debts. Capital and debts grow exponentially; that is, much faster than the real economy. However, this has profound social implications. You can read about that in more detail in the book. I was also very surprised that, in the standard economic textbooks I’ve read, very few economists have dealt with the topic. Actually, Keynes was the only mainstream economist I found who discussed the negative effects of our monetary and interest system in any depth. Interestingly, Keynes based his statements on findings by the economic maverick Silvio Gesell. Gesell had already written about the deficiencies of our monetary system 100 years ago! Nonetheless, university professors were not concerned with the redistribution of capital through positive interest rates. That situation has changed a little bit. For example, Professor Jürgen Kremer has recently proven my assertions with the help of long-term calculation models.

What do you expect from the English edition of the book?

I hope that social activists, environmentalists, and economists will gain new insights when reading the book. My work illustrates that systematic errors inherent in our monetary system prevail. These must be removed to effectively promote social justice and environmental sustainability. Next, I hope that The Money Syndrome will contribute to the discussion about ways to promote interest rates oscillating around 0%. Such a discussion was launched last year by professors such as Greg Mankiw from Harvard and Willem Buiter from the London School of Economics. In saturated economies, 0% interest rates are not only necessary to stabilize economic activity, but also to prevent a further accumulation of capital and explosion of debts due to the compound interest effect. In short, I hope that the book will help spread the knowledge about how economic stability, social justice, and peace in this world are essentially threatened by systematic errors in our monetary system. Our future survival requires that we recognize this mistake and correct it!

The interview was kindly provided by Felix Spira

Welcome

September 23rd, 2009

to our homepage dedicated to the work of Helmut Creutz about the basics of our monetary system. I’m happy to announce that the English edition of THE MONEY SYNDROME is now available. The German version of this book “Das Geldsyndrom” was first published in 1993 after twelve years of research that the author Helmut Creutz had undertaken. Since then thousands of readers got acquainted with his findings and the book became an indispensable work of reference for all those, who are convinced that our economic system should be thoroughly reviewed and reformed.

THE MONEY SYNDROME mainly deals with the German national economy since the end of World War II with a few side glances at other national economies. The English speaking reader might consider the emphasis on the German situation a disadvantage of the book. And yet there is another aspect which might make it worthwhile to have a closer look at Germany’s economic development.

In 1948 the German economy virtually started at point zero. There was little left, that could be used as a basis for the reconstruction of the country. It was mainly based on the strong willingness of its inhabitants to get back as soon as possible to a decent and worthwhile lifestyle. The economic development went through an “economic miracle” during the 1960ies until the mid-seventies when the first signs of a saturated economy appeared. The development of Germany’s economy was straight and clear, there have been no major deviations from the capitalist way despite an accent on social market economy and it managed to become one of the leading industrial nations.

The rise and fall of the German economy during the past 60 years is the textbook story of a capitalist society.

The presented material in THE MONEY SYNDROME – economic figures, tables, graphs and charts – allow the distinction of the various stages a capitalist economy is going through. On the example of Germany’s economy the effects and their causes become clear, which in a less comprehensive development of other economies may not be identified as precisely as in the German example, because the various phenomena are associated with assumptions or ideological convictions that may lead astray.

Today we are facing a financial crisis the dimension of which surpasses everything that has been known up to now. We are looking in the abyss of unprecedented squalor and corruption on the one side and on the other side sheer helplessness and fear. It’s time to go to the very roots of economic activity and remember what economy should actually be: a solid basis for a sound culture that respects human rights and dignity and facilitates prudent dealings with the natural environment on planet earth. The “real existing” socialism and capitalism have failed to provide this basis.

THE MONEY SYNDROME offers uncountable stimulations for a genuine new thinking.

Posted to “TechRepublic” today: http://www.techrepublic.com/article/silicon-valley-cto-explains-why-trump-happened/?ftag=TRE-00-10aaa0b&bhid=26535675722993845173453126631561#postComments

I certainly hope that advancing technology eliminates more “jobs”–that is what it is designed to do, i.e., replace labour with non-labour factors of production. The purpose of economics is to produce goods and services as, when and where required or desired–with maximum efficiency and minimal inconvenience for all concerned–not to create work. Life is more than bread alone.

The problem is widespread adherence to a Puritanical philosophy that demands human effort as a qualifier for partaking in consumption. This is totally irrational if non-labour factors are increasingly the source of produced wealth. We have demonstrated the capacity to produce evermore vast and varied goods and services. They were meant to be accessed and used by consumers to the extent desired. To the extent that there is a surfeit we should be able to revert to leisure.

Conventional industrial cost-accountancy as it interacts with the issue and cancellation of credit by the banks results in a growing deficiency of effective consumer purchasing-power compared with financial costs and prices in each costing cycle. Increasingly we resort to financial debt as an inflationary mortgage upon future production in order to make the system “work”. The more the replacement of labour by technology, the greater the disparity between prices and incomes. This requires us to engage in more and more production to earn the incomes required to purchase not current but past production. Even endless production of war materials is insufficient to “fill the gap” and consumer must resort even more to debt in order to claim the products of industry. Those individuals displaced from financially remunerative activity cannot qualify for loans. We have a phenomenal capacity to produce but live in world of want, waste and destruction.

Obviously we require a mechanism to distribute goods and services and if wages, salaries and dividends are insufficient then they must be supplemented by an additional form of income that does not form a claim against future earnings. We need a system of National (Consumer) Dividends and Compensated (Retail) Prices, financed not by debt but merely by withdrawals from an actuarially determined National Credit Account, being an estimated evaluation of the real credit of the nation, i.e., all of the real assets which if used for production would result in the creation of prices. The NCA would always be growing as all new capital assets were being credited to it.

The late British engineer Major Clifford Hugh Douglas anticipated all of these problems–which are actually untold blessings if properly considered–as early as 1918 and continued expostulating on the subject until 1951 in various books, pamphlets, addresses, broadcasts and journals. Because he challenged the fraudulent claim of the banking system to actual ownership of the financial credits which they issue as debt to monetize the real credit of the community–although they do not create the real wealth of society–his ideas were widely suppressed.

https://www.youtube.com/watch?v=ivfdcpB_fmg

www.socred.org

www.social-credit.blogspot.ca

www.socialcredit.com.au

https://www.youtube.com/watch?v=aUN_1mhXNLo

https://www.amazon.com/Social-Credit-Philosophy-Oliver-Heydorn/dp/1530390923?ie=UTF8&*Version*=1&*entries*=0

https://www.amazon.com/Social-Credit-Economics-Oliver-Heydorn/dp/1493529765

https://www.amazon.com/Economics-Social-Credit-Catholic-Teaching/dp/1494946262/ref=pd_bxgy_14_img_2?ie=UTF8&refRID=N82A1EGWQ489F2A16J03

https://en.wikipedia.org/wiki/Social_credit

Major C.H. Douglas on “Causes of War” – part 1 – YouTube

Major C.H. Douglas on ‘The Causes of War’ – part 2 – YouTube

http://social-credit.com/index.html

Wally Klinck

Avec mes meilleures salutations.

François de Siebenthal

Krach ? Solutions…

http://monetary.org/2008schedule.html

http://iousathemovie.com/ http://michaeljournal.org

http://desiebenthal.blogspot.com/

http://ferraye.blogspot.com/

skype siebenthal

00 41 21 652 54 83

021 652 55 03 FAX: 652 54 11

CCP 10-35366-2

Commentaires récents